Control your cover

Helping people like you with cover affordability

Your life insurance represents our promise to be there for you when it matters most, so it’s important you understand the ins and outs of your cover, and how to alter it, to keep up with your life changes too.

One of our jobs as an insurer is to ensure that the premiums collected are of a level to ensure claims can be paid. This means that we continue to monitor pricing and claims experience, across all products. Occasionally, we have to reprice our products to reflect changes in the cost of providing cover, so that we can keep you covered long term and maximise our ability to pay claims. Paying claims remains our unwavering priority and means our premium rates must reflect our true cost of providing protection.

At each anniversary, your premium may change. There are four main reasons that affect the cost of your premium…

![]()

1. Premium rate

adjustment

The cost of providing cover has increased across the industry.

![]()

2. Age

increases

As we age our risk of illness and death increases.

![]()

3. Inflation

protection

Your cover includes automatic indexation increases, to protect you against inflation.

![]()

4. Policy

duration

Premiums are generally lower if we've recently checked the life insured's health, financial and occupation status.

![]()

Other factors

Your premium may vary due to your payment frequency and levels cover.

*Premium illustration is representative only and not to scale.

The in-built management fee increases annually on the anniversary of your policy.

Life insurance cover is designed to move with you through life as your circumstances change. It makes sense to check your cover regularly to make sure you are getting the maximum value from your insurance. Find out more in the videos below.

Get maximum value from your insurance

Your life insurance is flexible and can be adapted to your changing needs. Make sure you have a cover review with your adviser every 12-18 months to ensure you’re covered or when major life events occur, for just the right amount, paying the right amount, and getting the best value from your policy.

The biggest advantage every policyholder should know

Once you’ve taken out fully-underwritten life insurance, your policy terms and conditions cannot be reduced and your policy can’t be cancelled by an insurer. In fact, once you’re covered, benefits can only move in your favour.

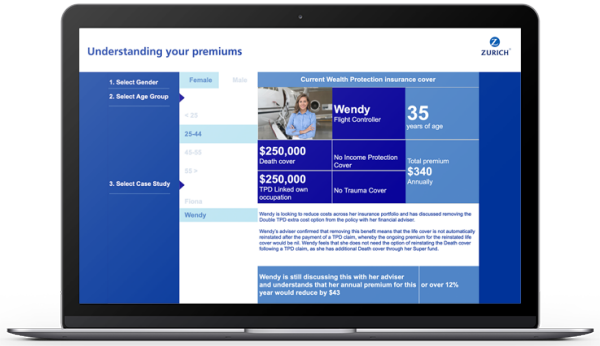

How you can control your cover

These two customer recognise the value of insurance and understand how vital it is to financial security. However, cost of living pressures are a concern.

Explore how Priyanka and Brian can reduce the cost of life insurance and make it more affordable.

We’re committed to supporting you through changing life circumstances by offering a range of options to alter your cover to assist with premium affordability.

The options available will vary by a number of factors, so we’ve put together some examples so you can see how people like you can reduce their premium.

We're here to help

If you are experiencing financial hardship or you’re concerned about your premium, please talk to your financial adviser or call us to discuss the options available to you.

To get you started, here’s a list of some of the options that may be available to you depending on the cover you have.

Premium reduction

Premium reduction

Conditions apply for both cover suspension and premium reduction, so please speak with your financial adviser or contact us to find out more.

- Check if you are eligible for the Involuntary Unemployment Waiver where premiums may be waived for up to 3 months if you have been made redundant

- Remove some extra cost options you may have selected - there is a variety of extra cost options that you could have on your policy so you can check with us, or your adviser to see if they can be removed

- Lower your cover amount

- Adjust your payment frequency to annual or half yearly

- Take a cover suspension and pause your cover

- Apply for non smoker rates if you have quit smoking for more than a year

- Check if your Insurance cover is within or linked to superannuation

- Switch off inflation protection (which indexes your cover amount) at each policy anniversary

- Explore the opportunity for tax deductions for your premiums.

- See if you are eligible to remove any premium loadings on your policy

Premium holiday

Premium holiday

A cover suspension allows for a break in cover for up to 12 months, to ease financial pressure.

Product Specific Options

Product Specific Options

Income Protection

- Reduce your benefit period on your income protection policy (i.e. the total amount of time you may be eligible to claim income protection benefits)

- Extend your waiting period on your income protection policy (i.e. the time you must be disabled before benefit payments start)

- (If applicable) Change from agreed value to indemnity cover

TPD

- Change the type of Total and Permanent Disablement (TPD) cover you have from Platinum TPD to standard TPD cover OR from Own occupation cover to Any occupation

Trauma

- Change the type of Trauma cover you have from Platinum to Extended Trauma cover

Additionally, you can contact us.

While we can’t talk to you about your personal circumstances in the same way your adviser can, we can talk to you about your policy, and the options available under your policy.

My Zurich is a portal where you can see your policy details, including what you're covered for.

Alan’s Terminal Illness Claim Story

"I now look back on how important that day was where Barry advised me to go with the Zurich life insurance…"

Annette’s Total and Permanent Disability (TPD) Claim Story

"The Zurich claims team helped me organise a TPD claim payout with surprising simplicity… "

We find ways to pay claims, not ways to deny them

Zurich retail supported 2,738 Life Insurance customers when it mattered most in 2023. Which gives you the confidence that if things go wrong, we will be there for you.

Total Claims Paid

$830 million

At Zurich, our philosophy is based on the simple belief that when our customers need us most, we are there.

We are proud of our excellent reputation and record in paying claims as quickly and transparently as possible, while providing the support and understanding that such difficult times deserve. We are committed to being Australia’s most trusted life insurer, backed by a strong global brand and a professional and growing team that has been recognised by the industry for its compassionate, transparent approach.

Speed and transparency

in paying claims

Strong

reputation

Focus on

customer care

Dedicated

people

Additional resources from moneysmart.gov.au to help you manage your finances:

- Budget Planner - work out where your money is going

- Managing Debt - get on top of debt and find help if you need it

- COVID-19 financial assistance - government support if you're impacted by coronavirus

Explore how you can reduce the cost of life insurance and make it more affordable.

View your policy online

Check your policy details and see what you're covered for.

Keeping you protected

If you’re concerned about your premium, please talk to your financial adviser. They can work with you to see if it makes sense for you to adjust your cover.

Additionally, you can contact us. While we can’t talk to you about your personal circumstances in the same way your adviser can, we can talk to you about your policy, and the options available under your policy.

Need help finding an adviser?

Zurich provides a free service that can connect you to an independent financial adviser:

ASIC’s MoneySmart website also has valuable information on what to look for when choosing a financial adviser.