Airlines were the first to be impacted during this crisis and are likely to be the last to get back to full operating capacity. I’d expect to see our states being slow to lift their “no travel” bans across borders and international travel being even slower to reignite. Why? Because looking at the COVID-19 maps, most infections originated from overseas travellers and it seems that the virus has not really spread to most of the developing world in a big way yet. When it does, their meagre health infrastructure will be totally inadequate to “flatten the curve”, no one will believe the reports on infection rates and local authorities will be very concerned about porous borders and the risk of a second wave of infection.

Can the airlines survive? Prudent capital raising and government support will likely ensure Qantas does. I would not be so confident about other domestic airlines or low-cost carrier models around the world.

On top of the developing world, the US is closer to a peak but its capitalist version of healthcare means it will likely suffer from a large number of unreported and untreated cases. Stories have emerged of US states bidding against each other for ventilators. As for the President’s bold prediction of being open for business by Easter, I am reminded of The Castle. “How much does he want for the jousting sticks... tell him he’s dreaming.” Christmas might be closer to the truth.

Locally, the National Cabinet has done a good job of containing the spread and number of deaths from the virus, but runs the risk of making the cure worse than the disease. It is incredible that it was only at the very end of March that advice was issued for people over 70 and those with chronic health problems to self-isolate. Given the earlier evidence from China and Europe that this was where 90%+ of the high-risk cases occurred, it should have been one of the early measures adopted. (Always easy in hindsight).

The Federal Government’s $130b package of wage subsidies is almost beyond belief in its scale. As Macquarie Research point out if you exclude the mining and building sectors which continue to function relatively normally, it represents about half the national wages bill over the next 6 months. It will take many years of prudent fiscal management to repair this scale of budget damage. In total, support measures represent an almost unimaginable 15%+ of GDP. This is surely approaching the limit of what can be done by Government.

What is being done on the monetary policy front? The most recent RBA minutes indicate members had “no appetite for negative interest rates“. While this is consistent with previous statements, it’s notable that the Board didn’t appear to have discussed purchases of corporate bonds. Given the huge blow-out in spreads and the need for many Corporates to refinance, I expect the Bank may be forced into buying this type of debt directly.

Before we Get to the Other Side

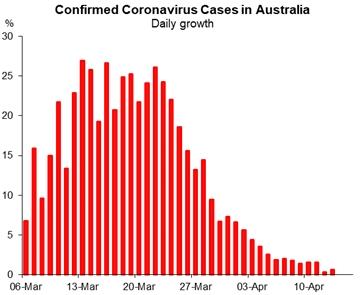

Lessons need to be learned from the Spanish flu pandemic in 1919 which had 3 separate phases where the infection rates spiked. Clearly the lesson here is not to remove social distancing protocols or lockdown provisions too soon. The risk is the clear flattening of the curve we are currently seeing in Australia could be transitory.

Daily growth in confirmed COVID-19 cases in Australia in percentage terms