- China’s lockdowns affect private consumption and housing demand, while industrial activity and infrastructure investment remain solid

We believe public support for the economy will accelerate and stick to our 2022 GDP growth forecast of 5.2% for now.

- ECB confirms QE to end in Q3, but also hints at spread control programme

The ECB`s confirmation that it plans to end QE in Q3 prepares the ground for eventual rate rises in Q4.

- Inflation accelerates in Argentina, reaching 16.1% YTD, while the Central Bank of Argentina (BCRA) hikes the reference rate by 250bps.

The jump in food prices was the main driver of the 20-year record monthly jump in CPI in March, while upward inflation pressure will remain during the following months.

Weekly Market Update

Investments

| Article

| 19 Apr 2022

|

Weekly Macro & Markets View

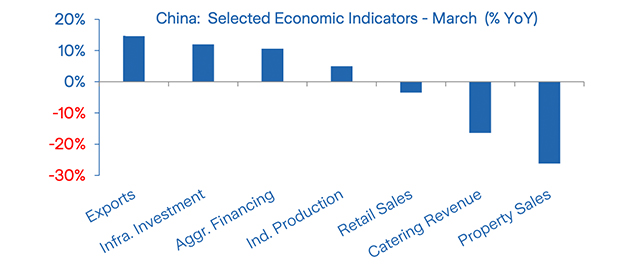

China’s consumption and property market activity nosedive in March

Source: NBS, PBoC, Barclays, Nomura, Bloomberg

At 5.3% in sequential annualised terms, China’s economy grew at a quicker pace than consensus had expected in Q1 and was up 4.8% YoY. This strong number masks the severe deterioration in March, as China is experiencing the worst Covid-related lockdowns since the Wuhan crisis, with more than one quarter of the population and GDP affected. The situation is particularly severe in the province of Jilin and in Shanghai, where the lockdown even seems to have caused public unrest. Clothing sales tumbled 12.7% YoY, auto sales were down 7.5% and catering revenue plunged 16.4%. Property was severely impacted as well, with the downturn accelerating. Property sales declined 26.2% YoY, new housing starts dropped 22.2% and land sales plunged 41%. The surveyed jobless rate rose from 5.5% to 5.8%.

Several well-respected economists are now cutting their 2022 growth forecasts to the 4- 41⁄2% range. We maintain our 5.2% projection for now as industrial activity and infrastructure investment are holding up much better than consensus had expected, while fiscal and monetary support is likely to accelerate. Even though the RRR cut by 25bps was smaller than expected, the quantity of liquidity provision should support the economy. However, we would need to revise our growth forecast lower should lockdowns extend and expand further.

US: Volatility in both data and markets

The holiday-shortened week provided a rollercoaster ride on both the data and market front. While equities oscillated day to day, the S&P 500 ultimately closed the week down just over 2%. The moves in Treasury yields were equally erratic. Mixed economic data sent 10yr yields down to 2.65% on Wednesday, before rebounding to 2.83%. The CPI inflation reading for March surprised positively. While the headline reading hit 8.5% YoY, the core rose only 0.3% on the month, despite sharp rises in airfares and shelter costs. Although this led to speculation of peaking inflation, a subsequent sharp rise in oil prices and jump in producer price inflation spurred the rebound in bond yields. Generally, the US economy remains in decent shape. Industrial production and capacity utilisation both showed improvement in March, and there were higher revisions to retail sales for Q1. Preliminary consumer sentiment for April also rebounded, while inflation expectations for one and five years out were flat. We continue to expect a 50bp hike by the Fed in May.

Eurozone: ECB confirms end of QE in Q3, but also hints at spread control if needed

At last week`s ECB monetary policy meeting and press conference, it confirmed plans to end QE asset purchases in Q3. Indeed, the ECB said that incoming information received since the last monetary policy meeting had reinforced its expectation that asset purchases should be concluded in Q3. At the same time, however, ECB President Christine Lagarde, was non-committal on which month QE would end, saying it could be July, August or September. In addition, Lagarde also said that the ECB was looking at possible measures to deal with so called fragmentation risk, i.e. a widening in periphery bond spreads, if needed. Overall, we expect QE net asset purchases to end in Q3, followed by two 25bps rate increases in Q4, taking the deposit rate to zero by the end of 2022. Meanwhile, the latest ECB bank lending survey showed a tightening in credit standards to enterprises in Q1, but a still healthy amount of loan demand. The tightening in lending standards is not yet at particularly high levels but needs monitoring as it is often a leading indicator for the wider economy.

APAC: Various central banks moving toward a more hawkish stance

Contrary to China’s 25bps RRR cut and stable monetary policy by the Bank of Japan and Bank Indonesia, other APAC central banks have become more hawkish. The Reserve Bank of New Zealand hiked its policy rate by 50bps to 1.5%, while consensus had expected only a 25bps hike. Governor Adrian Orr commented today: “We’ve provided strong forward guidance that we expect to be doing more rate rises over coming quarters”. Australia’s RBA seems to be taking the same approach, after having given up its ‘patient’ stance. In the April Minutes released today, the RBA noted that core inflation is likely to have moved above its 2-3% target range in Q1 and that wage growth is also picking up. A rate hike in June appears now more likely than in Q3. The Bank of Korea lifted its policy rate by 25bps to 1.5%, earlier than expected. The Monetary Authority of Singapore also tightened monetary policy by changing the mid-point of its exchange rate policy band and increasing the appreciation rate slightly while warning that inflation risks remain elevated over the medium term.

LatAm: March CPI reaches 20-year record high in Argentina, while upward inflation pressures remain

In Argentina, headline inflation jumped by 6.7% MoM in March, the highest print since April 2002, mainly driven by food prices. Annual inflation accelerated from 52.3% to 55.1%. Core CPI also accelerated sharply, rising 6.4% MoM, while regulated prices increased 8.4% MoM. Following the CPI release, the central bank hiked the reference rate by 250bps to 47%, arguing that higher international food and energy prices due to the war in Ukraine were the main drivers for March inflation. In Mexico, President AMLO failed in his effort to restore state control of the electricity sector as the energy bill fell short of the two-thirds majority needed in the Lower House to change the Constitution. In Chile, the government presented a limited pension fund withdrawal bill to Congress to stop a broader pension funds withdrawal proposal. The limited proposal, which allows the withdrawal of 10% of pension savings but only for specific uses, including debt payments, failed to align the government coalition. The Lower House rejected both bills on Monday.

Credit: A lacklustre week for credit

Risk assets struggled to gain traction last week, and credit was no different as spreads widened. Investor pessimism was evident in outflows last week, with USD 4.5bn outflows seen from US IG funds and USD 4bn outflows from US HY funds. Primary market activity was subdued too with the lowest US IG issuance since early February and the lowest YTD in Europe. New deals got a cold welcome: according to Bloomberg on April 12 average new issue concessions were 20 bp, more than double the YTD average, and order books were only 1.5 times covered, almost half the YTD average. High Yield primary markets also remain subdued. Last week’s price action shows that despite some encouraging signs which emerged previously in credit markets, investor sentiment still seems fragile. That said, we do sense a renewed resilience in credit in contrast to early 2022, given that the market has digested, without much damage, the substantial rise in Treasury yields. This implies to us that investor pessimism may be overdone and light positioning could cause credit resilience to continue.

What to Watch

- US housing data will capture attention in the coming week, with expectations for some slowing in all three metrics of building permits, housing starts and existing home sales, while PMI readings for April are expected to be largely unchanged.

- In the Eurozone, French Presidential Candidates, Emmanuel Macron and Marine Le Pen engage in a televised debate on Wednesday 20 April, followed by the actual polls taking place Sunday 24 April.

- In APAC, export data for March will be reported in Japan, Taiwan, and several ASEAN countries, while March CPI data will be released in Japan, Hong Kong, and Malaysia. Markets will be closed in Malaysia on Wednesday.

Disclaimer and cautionary statement

This publication has been prepared by Zurich Insurance Group Ltd and the opinions expressed therein are those of Zurich Insurance Group Ltd as of the date of writing and are subject to change without notice.

This publication has been produced solely for informational purposes. The analysis contained and opinions expressed herein are based on numerous assumptions concerning anticipated results that are inherently subject to significant economic, competitive, and other uncertainties and contingencies. Different assumptions could result in materially different conclusions. All information contained in this publication have been compiled and obtained from sources believed to be reliable and credible but no representation or warranty, express or implied, is made by Zurich Insurance Group Ltd or any of its subsidiaries (the ‘Group’) as to their accuracy or completeness.

Opinions expressed and analyses contained herein might differ from or be contrary to those expressed by other Group functions or contained in other documents of the Group, as a result of using different assumptions and/or criteria.

The Group may buy, sell, cover or otherwise change the nature, form or amount of its investments, including any investments identified in this publication, without further notice for any reason.

This publication is not intended to be legal, underwriting, financial investment or any other type of professional advice. No content in this publication constitutes a recommendation that any particular investment, security, transaction or investment strategy is suitable for any specific person. The content in this publication is not designed to meet any one’s personal situation. The Group hereby disclaims any duty to update any information in this publication.

Persons requiring advice should consult an independent adviser (the Group does not provide investment or personalized advice).

The Group disclaims any and all liability whatsoever resulting from the use of or reliance upon publication. Certain statements in this publication are forward-looking statements, including, but not limited to, statements that are predictions of or indicate future events, trends, plans, developments or objectives. Undue reliance should not be placed on such statements because, by their nature, they are subject to known and unknown risks and uncertainties and can be affected by other factors that could cause actual results, developments and plans and objectives to differ materially from those expressed or implied in the forward-looking statements.

The subject matter of this publication is also not tied to any specific insurance product nor will it ensure coverage under any insurance policy.

This publication may not be reproduced either in whole, or in part, without prior written permission of Zurich Insurance Group Ltd, Mythenquai 2, 8002 Zurich, Switzerland. Neither Zurich Insurance Group Ltd nor any of its subsidiaries accept liability for any loss arising from the use or distribution of publication. This publication is for distribution only under such circumstances as may be permitted by applicable law and regulations. This publication does not constitute an offer or an invitation for the sale or purchase of securities in any jurisdiction.