- Oil prices surge 20% on the week and stocks tumble as the war inUkraine intensifies

While the price of oil is still some way off from the USD 146 it hit back in 2008, the move will have a material impact on inflation and growth prospects, and it will take time for producers and consumers to adapt.

- Natural gas prices also spike, hitting record highs in Europe

High natural gas prices will weigh onthe Eurozone recovery and push inflation even higher. The key will be for how long energy prices stay elevated.

- US nonfarm payrolls rise by a solid 678’000 in February as workers rejoin the labour force

Despite the unemployment ratedropping to a post-recession low,average hourly earnings were flat ona monthly basis, removing somenear-term pressure from the Fed.

Weekly Market Update

Investments

| Article

| 07 Mar 2022

|

Weekly Macro & Markets View

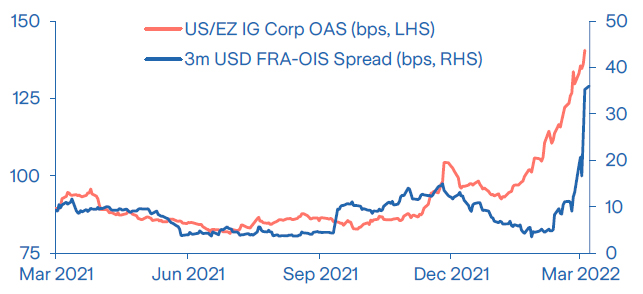

Credit sentiment knocked, but no signs of crisis yet

Source: Bloomberg

Note: Global OAS is 50% US and 50% European Corp Index OAS.

Credit markets suffered last week and are opening weak today amid surging energy prices and tumbling Russian assets. Negative sentiment was primarily driven by additional sanctions being placed on Russia and the Russia-Ukraine conflict becoming more protracted. Europe led the sell-off in risk assets with banks coming under stress as European bank stocks dropped by over 18% last week after having already fallen by nearly 9% the previous week. Credit derivatives underperformed corporate bonds as hedging activity gained momentum, while financials underperformed corporate credit. Notably, however, the US energy sector outperformed with spreads tightening over the week due to high oil prices. Indeed, elevated oil prices amid tightening monetary policy have increased risks to economic growth with sanctions on Russia’s energy imports currently being under review. That said, there are few signs of crisis in credit markets as of yet. The European banking sector linkages to Russia and Ukraine remain manageable, although they are much larger for the Eastern European economies, which could pose risks if the Russia-Ukraine conflict broadens out. FRA-OIS funding spreads, an indicator of banking sector stress, picked up but still remain far below crisis levels. All in all, while risks have risen notably, a credit bear market seems unlikely.

Markets: Stocks plunge, with those in Europe under acute pressure

The intensification of the war and the shelling of Europe’s largest nuclear power plant sent markets reeling, with the Euro STOXX index down 7% on the week and the German DAX down over 10%. 10yr Bund yields are back in negative territory, but the move lower in global yields was still relatively modest given the jump in risk aversion. We have noted before that investors have historically looked beyond conflicts, however, this time could be different as resolution looks protracted. The key issue for markets is the jump in commodity prices and the resulting impact on growth and inflation. Although oil prices remained above USD 100 from 2011 to 2014, the pace of the recent move and impact from other commodities is destabilising. It is not only oil, gas and grain prices that have surged, but also a number of critical components from Russia and Ukraine that support global supply chains. These include neon gas for chip production, palladium for catalytic converters in cars and nickel for batteries. With market conditions fraught, only better news flow on the conflict can turn investor sentiment.

US: The unemployment rate falls to a post-recession low

Nonfarm payrolls rose by a solid 678’000 in February reflecting the current strength of the labour market. The participation rate ticked up again as more workers join the labour force while the unemployment rate dropped to 3.8%, a new post-recession low. Despite the strong pickup in employment, average hourly earnings were flat compared to a month ago. This will help the Fed to start hiking rates at a moderate pace as indicated by Jerome Powell last week. The FOMC will keep its options open regarding the future rate path but soaring energy prices and their potential impact on growth and employment are likely to create a severe challenge for the central bank. Meanwhile, the latest ISM surveys show a reacceleration of manufacturing activity in February with a small tick down in price pressure. Services on the other hand faced more headwinds and expanded at a slower pace, reflecting the impact of Omicron, ongoing supply chain disruptions and challenges with hiring and retaining workers.

Eurozone: Unemployment falls, but high energy prices will weigh on growth

Business surveys published last week are starting to show an impact from rising geopolitical tensions and the associated jump in oil and natural gas prices. The Services PMI fell by around one point for Germany and around two points for France relative to the flash estimate. Since the survey was released, oil and natural gas prices have climbed even higher and at current levels are likely to be a substantial drag on growth in the region as well as push inflation higher. Inflation hit 5.8% in February, up from 5.1% in January, and this latest spike i n energy prices could push it well above 6% in March, weighing on consumers’ spending power. Producer price inflation also surprised to the upside in January, suggesting a pass through of previous energy price increases from the production chain. There is some resilience in the Eurozone economy as unemployment continues to fall, dropping from 7.0% in December to 6.8% in January. Governments are also likely to increase spending, but overall risks to the recovery have increased significantly in recent days.

China: Ambitious 5½% growth target suggests more policy stimulus

China’s Two Sessions (全国两会), comprised of the National People’s Congress (NPC) and the top political advisory body (CPPCC) meetings are underway. In his Government Work Report, Premier Li said China is facing the triple pressures of shrinking demand, disrupted supply, and weakening expectations. China’s growth target for 2022 was set at ‘around 5½%’, the lowest ever, but higher than what consensus had expected. We are now feeling even more comfortable with our above consensus growth forecast of 5.2%. As sequential QoQ growth rates need to be even higher to achieve the target, it is obvious that policy support will have to speed up further on the fiscal, monetary and administrative fronts. On a separate note, we are concerned about the dramatic surge of Omicron infections in Hong Kong, which is particularly affecting the large portion of unvaccinated elderly and is likely to be followed by severe lockdown measures. Mainland China has also registered a post-Wuhan high in new cases, suggesting that the dynamic zero-Covid policy will persist at least until year end.

APAC ex China: Topical bits and pieces across the region

Japan’s MoF survey showed solid corporate sales, profits and capex in Q4, but both the corporate outlook and consumer confidence have markedly deteriorated in the first two months this year. We expect a swift recovery in Q2 as the quasi state-of-emergency in most prefectures, amid the still high but receding new Omicron cases, is expected to end. In Australia, while the RBA recognises that inflation is coming in higher than expected, the fact that wage growth is still interpreted as being modest suggests to us that the ‘patient’ attitude will be maintained, and that the first policy rate hike can be expected for Q3. As Asian exports are concerned, we note that February export performance was brisk in China, South Korea, and Vietnam, which is encouraging. Moving to equity markets, the MSCI APEX 50 index fell 3.6% last week and retreated further today, pulling it down more than one third below its record high reached about a year ago.

What to Watch

- In the US, investors will focus on the latest set of inflation data while consumer sentiment is likely to remain muted.

- The ECB will meet to decide monetary policy. We expect that QE asset purchases will be tapered, but that policy flexibility and optionality will also be emphasised.

- We will closely watch China’s NPC and South Korea’s Presidential election during the week. In Japan, we will focus on the Eco Watchers Survey for February, while the revision for Q4 2021 GDP is likely to be small. In Australia, consumer confidence and inflation expectations for March will be released. In China, February export, inflation and credit data will be worth watching. Taiwan will report February export and inflation data.

- Annual inflation is expected to remain high in several countries in LatAm, with the core component likely to continue accelerating. Industrial production will be published in Brazil and Mexico, while retail sales in Brazil will be released. In Chile, the new government will take office on Friday.

Disclaimer and cautionary statement

This publication has been prepared by Zurich Insurance Group Ltd and the opinions expressed therein are those of Zurich Insurance Group Ltd as of the date of writing and are subject to change without notice.

This publication has been produced solely for informational purposes. The analysis contained and opinions expressed herein are based on numerous assumptions concerning anticipated results that are inherently subject to significant economic, competitive, and other uncertainties and contingencies. Different assumptions could result in materially different conclusions. All information contained in this publication have been compiled and obtained from sources believed to be reliable and credible but no representation or warranty, express or implied, is made by Zurich Insurance Group Ltd or any of its subsidiaries (the ‘Group’) as to their accuracy or completeness.

Opinions expressed and analyses contained herein might differ from or be contrary to those expressed by other Group functions or contained in other documents of the Group, as a result of using different assumptions and/or criteria.

The Group may buy, sell, cover or otherwise change the nature, form or amount of its investments, including any investments identified in this publication, without further notice for any reason.

This publication is not intended to be legal, underwriting, financial investment or any other type of professional advice. No content in this publication constitutes a recommendation that any particular investment, security, transaction or investment strategy is suitable for any specific person. The content in this publication is not designed to meet any one’s personal situation. The Group hereby disclaims any duty to update any information in this publication.

Persons requiring advice should consult an independent adviser (the Group does not provide investment or personalized advice).

The Group disclaims any and all liability whatsoever resulting from the use of or reliance upon publication. Certain statements in this publication are forward-looking statements, including, but not limited to, statements that are predictions of or indicate future events, trends, plans, developments or objectives. Undue reliance should not be placed on such statements because, by their nature, they are subject to known and unknown risks and uncertainties and can be affected by other factors that could cause actual results, developments and plans and objectives to differ materially from those expressed or implied in the forward-looking statements.

The subject matter of this publication is also not tied to any specific insurance product nor will it ensure coverage under any insurance policy.

This publication may not be reproduced either in whole, or in part, without prior written permission of Zurich Insurance Group Ltd, Mythenquai 2, 8002 Zurich, Switzerland. Neither Zurich Insurance Group Ltd nor any of its subsidiaries accept liability for any loss arising from the use or distribution of publication. This publication is for distribution only under such circumstances as may be permitted by applicable law and regulations. This publication does not constitute an offer or an invitation for the sale or purchase of securities in any jurisdiction.