- US business activity remains very robust with employment softening marginally

Both ISM surveys remain comfortably in expansionary territory while the drop in job openings and rising underemployment are further signs of a slightly less tight labour market.

- Lockdowns in Shanghai and Beijing have ended as the trough of the economic downturn has been reached

A boost to infrastructure investment is likely to support the economy in H2, though it will be difficult to achieve the government’s growth target of 5 1⁄2% this year.

- Australia’s RBA increases policy rates by 50bps to 0.85%, higher than the consensus forecast of 25bps and our forecast of 40bps

As the majority of Australia's home loan market is based on variable interest rates, the rate hike will have an impact on the economy. We now believe the market has priced in too many hikes for 2022.

Weekly Market Update

Investments

| Article

| 07 Jun 2022

|

Weekly Macro & Markets View

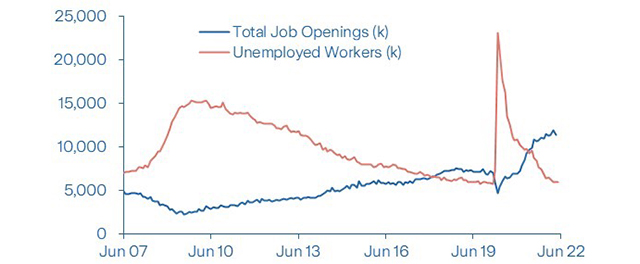

The Fed wants to shrink the gap between open jobs and unemployment

Source: Bloomberg

A whole range of economic data published last week paint a picture of slowing but still robust growth in the US. Both the ISM Manufacturing and ISM Services surveys remain comfortably in expansionary territory in May, at 56.1 and 55.9 respectively. In both cases, new orders have accelerated while prices paid ticked down but remain at very high levels, reflecting continuing price pressure in the pipeline. The latest batch of employment data show that the labour market remains very tight though, reassuringly, wage growth has not accelerated from month to month and has actually slowed from 5.5% to 5.2% on an annual basis. The Fed’s difficult task of cooling the economy and bringing inflation down without causing a significant rise in unemployment rests on decreasing the gap between job openings and the number of unemployed workers. The gap remains far above historical norms but the fact that job openings fell by almost 500’000 in April is a step in the right direction. Job creation slowed to 390’000 new payrolls in May with the unemployment rate remaining at 3.6% and the participation rate ticking up to 62.3%. Finally, consumer confidence softened in May driven by both the present situation and expectations with most sub-components showing reduced buying intentions in the months ahead.

Eurozone: Growth holds up, but inflation hits another record high

Eurozone data were mixed last week. The good news was further evidence of economic growth holding up in Q2 despite the Russian invasion of Ukraine. Although consumer confidence remains depressed, the European Commission’s overall Economic Sentiment indicator for May, which aggregates the industrial, service, consumer, retail and construction confidence indicators, was unchanged from April at 105. This level is consistent with a decent pace of economic growth in the region. However, the bad news was that Eurozone inflation surged to a fresh high of 8.1% in May from 7.5% in April. Worryingly, core inflation was also higher at 3.8% in May from 3.5% in April. While energy and food prices are the main reason for higher headline inflation, the rise in core inflation suggests previous increases in input costs and producer prices are gradually feeding through the production chain into consumer prices. Although we do not expect the ECB to raise rates at this week’s meeting, pressure to exit negative interest rates sooner rather than later is increasing.

Switzerland: Strong growth and inflation put pressure on the SNB

GDP surprised on the upside in Q1, rising by 0.5% QoQ or 4.4% YoY, with brisk industrial growth while services and construction activity was softer. Since then, leading indicators have moderated and point to trend-like growth in Q2, following a period with exceptionally strong activity. This has allowed supply pressures to come off their peaks, with the latest Manufacturing PMI showing an encouraging mix with softer input price pressures, a decline in order backlogs, and a tick higher in employment growth. CPI inflation was much stronger than expected in May though, with headline CPI up 0.7% MoM, taking annual inflation to 2.9%. While domestic price pressures remain benign, with services and domestic goods price inflation still tracking at around 1.5% YoY, this puts pressure on the SNB. Also considering that the ECB has accelerated its tightening path significantly, we expect the SNB to adjust their inflation forecast and signal a much more hawkish stance at next week’s policy meeting, but to leave rates unchanged for now.

Japan: Japan’s bumpy road to recovery

The latest series of economic indicators reveals a mixed picture. Industrial production has still been hampered by supply chain bottlenecks in the auto industry. However, despite the difficult economic environment, corporate sales and profits remained firm in Q1, as the MoF Corporate Survey revealed. However, this may change in Q2 as Japan’s exports to China have tumbled due to lockdowns in major cities and industrial areas and global demand is weakening. Companies still expect a sharp production rebound in May and June, but we think this view is too optimistic. On the positive side, consumption remains firm following the ebbing Omicron wave. Indeed, retail sales have reached the highest level since September 2019, the month before the consumption tax hike. However, even though the consumer confidence survey is encouraging, inflation expectations have risen to a record high and April data published today reveal that real wages have started falling again This will dent the positive outlook.

China: A patchy recovery is underway following the end of major lockdowns

The worst seems to be over in China as new Omicron infection cases are dwindling, lockdowns in Shanghai and Beijing have ended, and economic indicators are bottoming out. PMIs for May have recovered, though they remain below the boom/bust line of 50, indicating that China’s economic growth remains paltry at best, apart from large manufacturing companies showing a NBS PMI above 50. The push for stronger infrastructure investment continues, with the government providing an additional lending quota of RMB 800bn to public policy banks. This will help to stabilise growth in the second half of the year, provided no major lockdowns occur. Though there is a high-level political desire to reach the official growth target of 5½% this year, it is unlikely to be achieved by data mining, as an official campaign against manipulating statistics on a local level is underway. While the zero-Covid campaign will continue, excessive PCR testing by misusing public funds will be prosecuted. Meanwhile, both domestic ‘A’-shares as well as Honk Kong listed ‘H’-shares are recovering.

Credit: High Yield supply is coming back to life

Supply in High Yield credit, especially in the US, picked up last week after a long period of dull activity. We believe it is important, particularly for High Yield, that primary markets function well to preserve companies’ ability to fund themselves and keep default rates low. Flows into US High Yield showed the biggest inflows since June 2020, while European credit saw inflows as well, although US Investment Grade credit still saw outflows. US issuance in general picked up although the European primary market was slower due to public holidays. Even more importantly there was strong reception with some deals from US utilities seeing double-digit oversubscription, which is a significant improvement compared to the barely two times oversubscription level seen at times earlier this year. Credit spreads tightened on the week and were resilient even on Friday in the US despite the weakness seen in stocks after the US payroll report. All in all, it seems that credit markets continue to tentatively suggest a turn in sentiment.

What to Watch

- In the US, investors will be looking for confirmation as to whether inflation rates have peaked while consumer and small business sentiment are expected to remain subdued due to high price pressure.

- The ECB will meet to decide monetary policy this week. It is expected to confirm that net asset purchases will end early in July to prepare the ground for a rate increase at its July 21 meeting.

- In APAC, India’s RBI is expected to hike its repo rate by 50bps to 4.9%, while leaving its cash rate unchanged at 4.5%. Meanwhile, the probability of a rate hike by the Bank of Thailand has slightly increased. Mainland China and Taiwan will release export data for May, while several countries will publish May CPI data. Japan will release the Eco Watcher Survey for May, while South Korea will publish Q1 GDP data.

- In Chile, we expect the central bank to hike the policy rate by 75-100bps, stopping the tightening cycle, although inflation is not yet peaking. Annual inflation is expected to start to decelerate in Brazil and Mexico.

Disclaimer and cautionary statement

This publication has been prepared by Zurich Insurance Group Ltd and the opinions expressed therein are those of Zurich Insurance Group Ltd as of the date of writing and are subject to change without notice.

This publication has been produced solely for informational purposes. The analysis contained and opinions expressed herein are based on numerous assumptions concerning anticipated results that are inherently subject to significant economic, competitive, and other uncertainties and contingencies. Different assumptions could result in materially different conclusions. All information contained in this publication have been compiled and obtained from sources believed to be reliable and credible but no representation or warranty, express or implied, is made by Zurich Insurance Group Ltd or any of its subsidiaries (the ‘Group’) as to their accuracy or completeness.

Opinions expressed and analyses contained herein might differ from or be contrary to those expressed by other Group functions or contained in other documents of the Group, as a result of using different assumptions and/or criteria.

The Group may buy, sell, cover or otherwise change the nature, form or amount of its investments, including any investments identified in this publication, without further notice for any reason.

This publication is not intended to be legal, underwriting, financial investment or any other type of professional advice. No content in this publication constitutes a recommendation that any particular investment, security, transaction or investment strategy is suitable for any specific person. The content in this publication is not designed to meet any one’s personal situation. The Group hereby disclaims any duty to update any information in this publication.

Persons requiring advice should consult an independent adviser (the Group does not provide investment or personalized advice).

The Group disclaims any and all liability whatsoever resulting from the use of or reliance upon publication. Certain statements in this publication are forward-looking statements, including, but not limited to, statements that are predictions of or indicate future events, trends, plans, developments or objectives. Undue reliance should not be placed on such statements because, by their nature, they are subject to known and unknown risks and uncertainties and can be affected by other factors that could cause actual results, developments and plans and objectives to differ materially from those expressed or implied in the forward-looking statements.

The subject matter of this publication is also not tied to any specific insurance product nor will it ensure coverage under any insurance policy.

This publication may not be reproduced either in whole, or in part, without prior written permission of Zurich Insurance Group Ltd, Mythenquai 2, 8002 Zurich, Switzerland. Neither Zurich Insurance Group Ltd nor any of its subsidiaries accept liability for any loss arising from the use or distribution of publication. This publication is for distribution only under such circumstances as may be permitted by applicable law and regulations. This publication does not constitute an offer or an invitation for the sale or purchase of securities in any jurisdiction.