- ECB President Christine Lagarde hints strongly that the bank now plans to raise rates later this year

We now expect a faster wind down of QE asset purchases and at least one rate increase by the ECB in Q4, however the Eurozone economy should be able to cope with this.

- Nonfarm payrolls rise more than expected in January, prior two months are revised up significantly

Though last month’s labour market data were distorted by seasonal and population data adjustments they continue to reflect a strong employment situation.

- Government bond yields snap higher on hawkish central bank surprises

Some further upside to yields is possible, given a backdrop of strong growth and inflation and an improving Covid situation, but a pause for digestion now appears warranted.

Weekly Market Update

Investments

| Article

| 07 Feb 2022

|

Weekly Macro & Markets View

Lagarde refuses to rule out ECB interest rate increases later in 2022

Source: Bloomberg

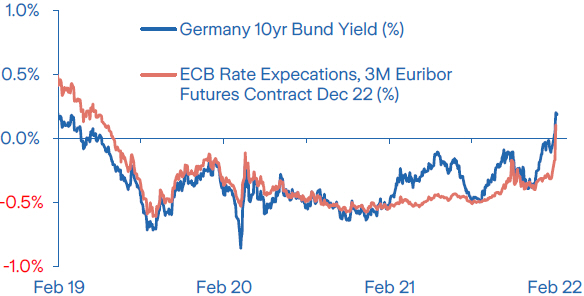

Following stronger than expected inflation data the ECB appears to be preparing to wind down QE asset purchases more quickly in order to raise interest rates later this year. In an important departure from previous statements, ECB President Christine Lagarde refused to rule out a rate increase this year during her monetary policy press conference last week. She also said that ‘there was unanimous concern around the table of the Governing Council about inflation numbers’.

Eurozone headline inflation increased from 5.0% in December to 5.1% YoY in January, much stronger than the consensus forecast of a fall to 4.4%. Technical factors, such as a temporary VAT cut in Germany coming out of the annual price comparison and the new inflation basket weightings, were not as favourable in terms of bringing inflation down as had been expected. Surging oil prices also pushed up energy inflation further. Whatever the reasons, this latest inflation print appears to have been the final straw for hawks within the ECB. We expect the ECB will announce formally at its March meeting that asset purchases will end in Q3, to prepare for at least one or possibly two 25bps interest rate hikes in Q4. We have long argued that negative interest rates are distortionary and counterproductive, so exiting them sooner is arguably no bad thing. However, the ECB will have to be careful that a tightening in financial conditions, especially in periphery economies, does not damage the recovery.

UK: The BoE further tightens its monetary policy

As expected, the Bank of England lifted the Bank Rate from 0.25% to 0.5% at its meeting last week. The move came with a hawkish tilt, though, as four of the nine members of the Monetary Policy Committee voted in favour of a 50bps move. The MPC voted unanimously to begin to passively reduce the stock of UK government bond purchases. As indicated earlier on, active sales will be on the radar once the Bank Rate has reached 1%. Despite the hawkish signal provided by the strong minority voting for a more pronounced rate increase, the underlying message was more muted. The BoE expects GDP growth to slow to subdued levels signaling that only some further modest tightening in monetary policy is likely to be appropriate in the coming months. Governor Bailey cautioned investors not to get carried away on the scale of tightening needed to get the economy back into equilibrium. Given all this, we expect the BoE to follow up with two more rate hikes in March and May followed by a pause with further steps dependent on economic development in the second half of the year.

US: Payrolls rise much more than expected

The latest batch of labour market data shows that 467’000 new nonfarm payrolls were created in January. In addition, the prior two months were revised up by more than 700’000. While these numbers are significantly higher than expected they have to be taken with a grain of salt as seasonal adjustments are likely to have significantly distorted the measures. Similarly, although it’s reassuring to see that the participation rate has increased markedly, revised population numbers are blurring the underlying picture. Nevertheless, the data reflect a strong employment situation. Further on, while average hourly earnings growth accelerated to 5.7% YoY in January, unit labour costs were almost flat in Q4 following a strong rise in Q3. Rising wages do not have to lead to higher inflation if productivity rises even faster as shown in Q4 last year. Business activity remains buoyant with both the ISM Manufacturing as well as the Services surveys well in expansive territory.

Australia: The RBA is getting more hawkish, but remains patient

The Reserve Bank of Australia (RBA) left its policy rate unchanged at 0.1% but announced that it will end its quantitative easing (QE) programme by the end of this week. Listening to Governor Lowe’s speech, we suspect that a first step toward quantitative tightening (QT) in the form of not re-investing proceeds of maturing bonds is likely to be announced when the RBA Board convenes in May. Some observers believe that this will quickly be followed by a policy rate hike, while the market had already priced in four rate hikes this year. We believe a first cash rate hike is rather likely for later this year, as Lowe admitted that a rate hike is ‘plausible’, but the RBA Board will remain ‘patient’. In Friday’s quarterly Statement on Monetary Policy (SMP) the RBA significantly lifted its inflation forecast. The trimmed-mean measure is expected to peak at 3.25% in Q2, one percentage point higher than previously expected, before falling back to 2.75%. The RBA also lifted its wages and average hourly earnings forecast, while cutting its GDP growth and unemployment forecasts.

Bonds: Government yields surge on hawkish central bank surprises

Bond yields surged on hawkish news from central banks, particularly from the ECB and the BoE. At 1.91%, the 10yr Treasury yield is back to its pre-Covid level, though remains well below the 3% reached in 2018. In Europe, core yields have overshot pre-crisis levels, with the 10yr Bund yield above 0.22% and upward pressure on peripheral yields. While a significant amount of rate tightening is now priced into the rates market, with over five 25bps hikes for the Fed and the BoE for the coming year and 2.5 hikes for the ECB, the long end of the curve is vulnerable to further upside, particularly as central banks begin to unwind asset purchases. Rising yields have reflected higher real yields while market inflation expectations have been flat or, in the case of the Eurozone, slipped back. Despite their snap higher, real yields are low compared to history and further upside is warranted given strong demand and inflation. While we anticipated yields would rise in 2022, the move has been more frontloaded than expected, particularly in Europe, and we suspect a pause to digest may be required.

Equities: Stocks struggle higher, as tech earnings paint a mixed picture

It was another turbulent week for equities, leaving markets broadly higher with the MSCI World Index up 1.9%. While investors digested the jump in bond yields, amid decidedly more hawkish central banks, high profile tech earnings captured the headlines given their violent impact on share prices. Halfway through the US Q4 results season numbers are robust, with 76% of S&P 500 companies beating estimates by around 8%. However, the fortunes of the mega-cap tech names were decidedly mixed. While the shares of Amazon and Alphabet (the parent of Google) surged on robust reports, Meta (formally known as Facebook) lost more than a quarter of its value in a day on disappointing numbers. This confirms our view that in a world of high valuations, rising interest rates, and shrinking liquidity, fundamentals will matter more than they have in recent years. This is healthy. We are also encouraged that investors appear to be adjusting to the new rising rate environment. While volatility will likely remain high, we do see signs of a bottoming pattern developing for equity markets.

What to Watch

- In the US, investors will focus on the latest set of inflation data while the University of Michigan’s Consumer Sentiment Survey will give important insights into the current state of US households.

- We expect the central banks of Indonesia, Thailand and India to keep policy rates unchanged, though there is a chance that the RBI may slightly hike its Reverse Repo Rate. China is likely to release money supply and credit data for January. In Japan, we will focus on the Eco Watchers Survey and corporate goods prices for January. Malaysia’s Q4 GDP as well as Taiwan’s export and inflation data for January will be released as well. Japan’s financial markets will be closed on Friday due to Foundation Day.

- In Mexico, the focus will be on the monetary policy meeting at which we expect Banxico to hike the policy rate by 50bps to 6%. Inflation for January will be released in Brazil, Chile, and Mexico, key figures for the evolution of monetary policy.

Disclaimer and cautionary statement

This publication has been prepared by Zurich Insurance Group Ltd and the opinions expressed therein are those of Zurich Insurance Group Ltd as of the date of writing and are subject to change without notice.

This publication has been produced solely for informational purposes. The analysis contained and opinions expressed herein are based on numerous assumptions concerning anticipated results that are inherently subject to significant economic, competitive, and other uncertainties and contingencies. Different assumptions could result in materially different conclusions. All information contained in this publication have been compiled and obtained from sources believed to be reliable and credible but no representation or warranty, express or implied, is made by Zurich Insurance Group Ltd or any of its subsidiaries (the ‘Group’) as to their accuracy or completeness.

Opinions expressed and analyses contained herein might differ from or be contrary to those expressed by other Group functions or contained in other documents of the Group, as a result of using different assumptions and/or criteria.

The Group may buy, sell, cover or otherwise change the nature, form or amount of its investments, including any investments identified in this publication, without further notice for any reason.

This publication is not intended to be legal, underwriting, financial investment or any other type of professional advice. No content in this publication constitutes a recommendation that any particular investment, security, transaction or investment strategy is suitable for any specific person. The content in this publication is not designed to meet any one’s personal situation. The Group hereby disclaims any duty to update any information in this publication.

Persons requiring advice should consult an independent adviser (the Group does not provide investment or personalized advice).

The Group disclaims any and all liability whatsoever resulting from the use of or reliance upon publication. Certain statements in this publication are forward-looking statements, including, but not limited to, statements that are predictions of or indicate future events, trends, plans, developments or objectives. Undue reliance should not be placed on such statements because, by their nature, they are subject to known and unknown risks and uncertainties and can be affected by other factors that could cause actual results, developments and plans and objectives to differ materially from those expressed or implied in the forward-looking statements.

The subject matter of this publication is also not tied to any specific insurance product nor will it ensure coverage under any insurance policy.

This publication may not be reproduced either in whole, or in part, without prior written permission of Zurich Insurance Group Ltd, Mythenquai 2, 8002 Zurich, Switzerland. Neither Zurich Insurance Group Ltd nor any of its subsidiaries accept liability for any loss arising from the use or distribution of publication. This publication is for distribution only under such circumstances as may be permitted by applicable law and regulations. This publication does not constitute an offer or an invitation for the sale or purchase of securities in any jurisdiction.