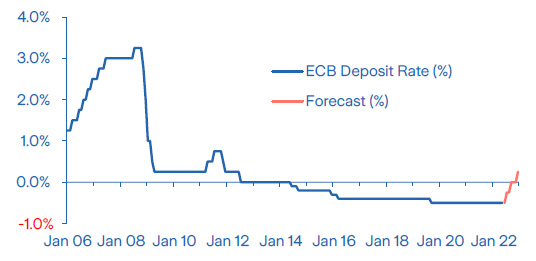

- In a blog posted on the ECB's website last Monday, President Lagarde says that it is planning to raise interest rates in July

An increase in interest rates by the ECB would be a tightening in financial conditions, but a few modest rate increases are unlikely to push the region into recession.

- The S&P 500 gains 6.6% following a long series of weekly losses

Investor sentiment got too pessimistic recently given slowing but solid growth, though potential headwinds remain, particularly given the Fed’s hawkish stance.

- Credit markets have become more resilient lately, with US credit spreads gapping tighter last week

Credit tends to lead other markets and the encouraging recent price action indicates that investor positioning has become too light amid excessive pessimism, tentatively suggesting a turn in sentiment.

Weekly Market Update

Investments

| Article

| 30 May 2022

|

Weekly Macro & Markets View

Lagarde reveals ECB plan to raise rates in July

Source: Bloomberg,ZIG

Last week, in a blog posted on its website, ECB President Christine Lagarde gave a clear indication that it is planning to raise interest rates by 25 basis points (bps) for the first time in 11 years at its July 21 meeting and then raise interest rates by another 25 bps at its September 8 meeting, so as to ‘exit negative interest rates by the end of the third quarter’. Lagarde also said that net QE asset purchases would ‘end very early in the third quarter’. The guidance by Lagarde was unusually direct, and her plans were confirmed by ECB Chief Economist Philip Lane in an interview this morning. We expect that there will be a further 25 bp rate increase at the ECB’s December 15 meeting.

The last time the ECB engaged in a rate-tightening cycle was in 2011 and before that in 2008, raising fears that it may be about to raise interest rates again just before another severe slowdown and recession. Although recession risks are high given the current geopolitical situation, we do not expect modest rate increases alone will tip the region into contraction. Indeed, we have long regarded negative interest rates as counterproductive because they create distortions in the financial system. Exiting negative interest rates should therefore be a good thing. Meanwhile, data released last week for the region were encouraging. The flash S&P Eurozone Composite PMI only declined modestly and was still consistent with a decent pace of growth in the second quarter.

US: The S&P 500 rebounds with a vengeance

Following the longest streak of weekly losses in more than two decades the S&P 500 rebounded with the biggest weekly gain since November 2020 (when positive news on vaccines against Covid lifted markets worldwide). The S&P 500 gained 6.6% (more than 9% above the intra-day low on May 20th) while the Nasdaq rose by 6.8%. There was no particular trigger for the rebound though market sentiment has turned very pessimistic recently. A number of positive earnings reports, the lack of a hawkish tilt to the Fed minutes, and a slowdown in annual PCE core inflation from 5.2% to 4.9% all helped to lift markets out of the doldrums. Meanwhile, economic data published last week continue to signal that growth is slowing but that fears of an imminent recession seem overdone. The housing market remains under pressure, though, with new home sales falling by 16.6% MoM in April, following a decline of 10.5% MoM in March. Given the visible impact of financial tightening on economic activity, investors have started to lower their expectations regarding the Fed’s terminal rate.

North Asia: China’s new stimulus measures are expected to stablilise growth in H2

China’s State Council launched a stimulus package comprising 33 measures to support the ailing economy. The measures include support for SMEs and individuals, the removal of supply chain bottlenecks, the launch of new construction projects, and an increase in coal output to improve energy security. Separately, initiatives to stimulate new vehicle purchases were initiated. Premier Li was quite outspoken about the negative impact of Covid related lockdowns and mass-testing on the economy and government finances. Meanwhile, new infections are receding, and Shanghai and Beijing will start returning to normality, though access to public venues will be controlled. In Japan, the Manufacturing PMI for May and its major components deteriorated amid the impact of disruptions in trade with China, while the Services PMI improved as consumer confidence is slowly improving following a reduction in new Omicron infections. The Bank of Korea hiked its policy rate by 25bps to 1.75%, raised its inflation outlook and cut its growth forecast.

LatAm: Equity markets continue their recent rebound

LatAm equity markets continued their recent rebound last week, showing a positive performance for the month of May, now at around 10% according to the MSCI LatAm Index, with the Chilean stock market leading the gains. Investors seems to be looking through recent political uncertainty, with the Constitutional Convention in Chile having recently delivered the first draft of the new Constitution, and now moving to a fine-tuning phase, with a referendum scheduled for September 4. Meanwhile, in Mexico the final GDP release for Q1 showed the economy grew 1% QoQ, in line with the preliminary estimate published one month ago and with both industrial production and the service sector contributing to growth. Finally, in Brazil, the Lower House approved a bill that labels fuels, electricity, gas, communications, and public transport as essential goods, implying a reduction in the state tax for these goods. The bill will now move to the Senate. The Economic Ministry expects this will translate to a BRL 0.7 per litre reduction in gasoline prices and also a reduction in diesel prices.

US Municipal Credit: First signs of stabilisation may be boosted by summer cash flows

Following one of the worst historical underperformances during the first several months of the year, US municipal bonds strongly outperformed Treasuries last week in one of the first broad-based rallies of 2022. Ratios between municipal and Treasury yields were particularly cheap when they climbed above 100% mid-May but have now retreated to around 91% for the 10yr tenor. Aside from the negative impact of higher Treasury yields and elevated volatility, municipal bonds have also suffered from very large outflows. There have been only three weeks of positive inflows this year and cumulative YTD net flows have now reached an impressive minus USD 37bn. We think that technicals will turn now and be more supportive with the seasonal summer surge in coupon payments and bonds redemptions. Municipal issuers should also benefit from good fundamentals as high inflation will increase tax collections and boost revenues for state and local governments. We think that current ratios may provide a good entry poinst for investors if the Treasury yields stabilise.

Credit Spread action emits encouraging signals

Credit markets are often considered a leading indicator for other markets. In this context, it is notable that the US credit market had been emitting some encouraging signs over the last couple of weeks, even before the latest bounce in stocks. We believe that the stability and resilience of credit is a consequence of a lightening of positions amid investor pessimism that may have become excessive. It was notable over the last two weeks that even during the days when stocks were volatile, credit spreads were resilient. Spreads gapped tighter last week, especially in the US High Yield market, including the weakest CCC segment seeing the largest weekly returns in 18 months. However, some signs of fragility still remain. Primary markets continued to remain subdued, with US Investment Grade credit seeing only one bond deal while outflows continue to be seen across credit funds. So all in all, while price action in credit has become encouraging, the strength needs to become more broad-based to be interpreted as evidence of a turn in sentiment.

What to Watch

- In the US, the ISM surveys are expected to reflect a further slowdown in growth while the latest batch of labour market data will give crucial insights into the current employment and wage situation.

- In the Eurozone, various economic data and surveys are likely to confirm that the region is still growing despite the various shocks it has experienced recently.

- For Switzerland, CPI, PMI, trade and GDP data will show how activity and inflation are holding up.

- In APAC, Japan will release April economic activity data on Tuesday. China will publish its May PMIs. South Korea will report statistics for April industrial production as well as May foreign trade and CPI data. India will release Q1 GDP statistics. Markets will be closed on Friday in China, Hong Kong, Taiwan and Thailand, as well as in Korea on Wednesday.

Disclaimer and cautionary statement

This publication has been prepared by Zurich Insurance Group Ltd and the opinions expressed therein are those of Zurich Insurance Group Ltd as of the date of writing and are subject to change without notice.

This publication has been produced solely for informational purposes. The analysis contained and opinions expressed herein are based on numerous assumptions concerning anticipated results that are inherently subject to significant economic, competitive, and other uncertainties and contingencies. Different assumptions could result in materially different conclusions. All information contained in this publication have been compiled and obtained from sources believed to be reliable and credible but no representation or warranty, express or implied, is made by Zurich Insurance Group Ltd or any of its subsidiaries (the ‘Group’) as to their accuracy or completeness.

Opinions expressed and analyses contained herein might differ from or be contrary to those expressed by other Group functions or contained in other documents of the Group, as a result of using different assumptions and/or criteria.

The Group may buy, sell, cover or otherwise change the nature, form or amount of its investments, including any investments identified in this publication, without further notice for any reason.

This publication is not intended to be legal, underwriting, financial investment or any other type of professional advice. No content in this publication constitutes a recommendation that any particular investment, security, transaction or investment strategy is suitable for any specific person. The content in this publication is not designed to meet any one’s personal situation. The Group hereby disclaims any duty to update any information in this publication.

Persons requiring advice should consult an independent adviser (the Group does not provide investment or personalized advice).

The Group disclaims any and all liability whatsoever resulting from the use of or reliance upon publication. Certain statements in this publication are forward-looking statements, including, but not limited to, statements that are predictions of or indicate future events, trends, plans, developments or objectives. Undue reliance should not be placed on such statements because, by their nature, they are subject to known and unknown risks and uncertainties and can be affected by other factors that could cause actual results, developments and plans and objectives to differ materially from those expressed or implied in the forward-looking statements.

The subject matter of this publication is also not tied to any specific insurance product nor will it ensure coverage under any insurance policy.

This publication may not be reproduced either in whole, or in part, without prior written permission of Zurich Insurance Group Ltd, Mythenquai 2, 8002 Zurich, Switzerland. Neither Zurich Insurance Group Ltd nor any of its subsidiaries accept liability for any loss arising from the use or distribution of publication. This publication is for distribution only under such circumstances as may be permitted by applicable law and regulations. This publication does not constitute an offer or an invitation for the sale or purchase of securities in any jurisdiction.