- The invasion of Ukraine by Russia marks a seminal moment for Europe

Orchestrated global sanctions are imposed on Russia as prospects for a speedy resolution fade. A jump in energy prices risks further upside to inflation.

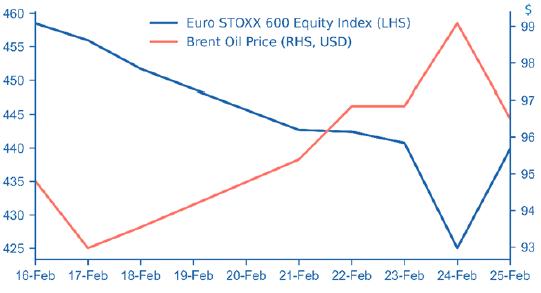

- Equity markets plunge as the invasion takes place, then bounce

Investors seem prepared to look through the conflict, given the relatively limited global economic consequences, and refocus on strong growth and earnings prospects that support equity returns.

- European credit bore the brunt of the investor angst arising from the Russia-Ukraine conflict

While the impact of the conflict oncredit spreads may not be long lasting, risks have increased while long-term headwinds are likely to cause fragile investor sentiment to persist.

Weekly Market Update

Investments

| Article

| 28 Feb 2022

|

Weekly Macro & Markets View

War in Europe sparks a twist in markets

Source: Bloomberg

The tragedy of war in Europe has again become a reality as Russian forces invaded Ukraine last week. Despite the inevitable human cost, investors took a dispassionate view of events as is so often the case in times of war. The sharp correction in financial markets as the invasion commenced reversed course when the tanks rolled in and sanctions were announced, with US stocks actually closing up on the week. Oil prices breached USD 100 intraday for the first time since 2014, before moderating slightly. The implication from markets was that Russia’s expansion would be restricted to the Ukraine and have a limited impact on global corporate profitability and the economic cycle. While the surge in energy prices will undoubtedly dent growth if they are maintained for a protracted period, economic conditions are generally robust and are likely to absorb the headwind. The inflationary impact is more concerning, coming at a time when inflation is already significantly above target on a global scale and forcing central banks to accelerate tightening. However, the conflict is likely to inject a degree of caution into the process, which investors appreciate. To us, despite the depressing human toll that is being borne, the old investor adage of ‘sell the rumour and buy the news’ is likely to drive stocks and bond yields higher bar further escalation, though the process will be bumpy.

Credit: Sentiment remains fragile

Credit markets were volatile last week and are opening weak this morning as Russia’s invasion of Ukraine has dented investor sentiment. While some stability returned to credit on Friday, further developments over the weekend such as new sanctions from the West and the prospect of a prolonged conflict have the potential to increase uncertainty further. Despite the notable weakness in corporate bonds, credit derivative indices fared better. Europe led the weakness in cash credit markets, given it’s relatively higher exposure to the Russia-Ukraine conflict. European bank credit underperformed as European bank stocks dropped by over 8% on Thursday alone. In contrast, US high yield saw spreads tighten over the week, led by the energy sector amid the rising price of oil. While geopolitical risk impacts tend to fade, the broader headwinds for credit are likely to persist, unless central banks change their stance notably. Consequently, sentiment is likely to remain fragile in credit for some time.

US: Strong growth and still surging inflation point the way for rates

Despite the dreadful developments in Ukraine, any doubts about a Fed rate hike in March were surely put to rest as a string of strong economic readings and a further jump in inflation were reported last week. House prices rose 1.5% in December and are up 18.6% on a YoY basis, while personal spending rebounded by 2.1% in January. Durable goods orders also surprised positively with strong revisions to prior data, but it was the PMI readings that caught our attention. While the manufacturing reading moved back up to 57.5, a five-and-a-half-point improvement in services to 56.7 implies a strong reopening of the service sectors as we had hoped. With the US economy in rude health a further jump in the Fed’s favoured PCE inflation readings makes a March rate hike a near certainty. Headline PCE was 6.1% YoY, with the core at 5.2% ⎯ a long way from the Fed’s 2% target. 10yr Treasury yields briefly breached 2% despite the geopolitical turmoil, while stocks closed the holiday-shortened week modestly higher, despite massive intra-week volatility.

Eurozone: Business surveys point to a rebound, but geopolitics will weigh

Various business surveys were released last week, all carrying a similar message. The region’s service sector economy is bouncing back as the Omicron wave fades, while supply-side disruptions are easing in the manufacturing sector. For example, the flash Eurozone PMI survey jumped more than four points from 51.1 in January to 55.8 in February, while manufacturing confidence remained at a robust level and supplier delivery times improved. The German ifo Business Climate index also rebounded sharply in February, while the European Commission’s Economic Sentiment indicator increased more than two points, with a four-point gain in the services subcomponent. However, these surveys were released before the invasion of Ukraine, which has led to a spike in oil and gas prices. This will increase inflation further and dampen real spending power, but we do not think that the current jump in energy prices is enough to completely derail the recovery.

Switzerland: GDP growth slows as expected, but the outlook remains favourable

GDP growth slowed from 1.9% in Q3 to 0.3% QoQ in Q4. The moderation was expected, partly reflecting a normalisation in growth dynamics after the reopening bounce-back, and partly due to headwinds from rising infections and renewed restrictions. The underlying details were solid, with brisk manufacturing activity despite supply chain issues and gains in consumption and investment. Government spending also bolstered growth. Looking forward, we expect activity to hold up well in 2022, with strong external demand and a healthy domestic backdrop likely to provide resilience amid the challenging geopolitical situation. Households are benefiting from the strong labour market and favourable financial conditions, as reflected in the latest retails sales data, which showed a rebound in January following some moderation in Q4. The KOF leading indicator finally ticked down in February but remains well above the historical average and is consistent with above-trend growth in the economy.

Japan: Omicron is hitting Japan’s consumption and production

We are not surprised that the retail sales and industrial production statistics released today for January came in weaker than consensus had expected. We have flagged before that the surge in Omicron cases as well as supply chain issues and labour shortages in the manufacturing sector would negatively impact Japan’s economy in Q1. Retail sales contracted 1.9% MoM following a downward revised contraction of 1.2% in December. Considering that services consumption is likely to have been hit even more seriously than goods consumption, we suspect that overall private consumption will contract in Q1. Industrial production contracted 1.3% MoM versus -1% in December, with motor vehicle production showing a substantial drop of 17.2% MoM. Companies project a recovery in February and March, but these forecasts tend to be too optimistic. However, we expect a strong rebound in Q2 as new Omicron cases are already falling and labour shortages should have subsided by then.

What to Watch

- Attention will turn to the US jobs data, which includes payrolls and the unemployment rate, with particular focus on the participation rate as an indicator that the supply of workers may be improving.

- In the Eurozone, the flash estimate of February inflation is likely to show a further jump because of energy prices. The final PMIs will also be important to watch to see how the latest escalation in geopolitical tensions has affected confidence.

- We do not expect any policy rate changes from Australia’s RBA or Malaysia’s BNM, but will watch for suggestions of potential hikes earlier than previously expected following stronger inflation prints. Australia will release Q4 GDP and January retail sales, exports, building approvals, private sector lending and February house prices. Japan will publish labour market data for January. China will release its February PMIs. South Korea will publish Q4 GDP, January industrial production and February export data.

- Q4 GDP will be released in Brazil, while monthly economic activity for January will be published in Chile. In Mexico, the focus will be on the inflation report, for which we expect downward revisions of growth and upward revisions of inflation.

Disclaimer and cautionary statement

This publication has been prepared by Zurich Insurance Group Ltd and the opinions expressed therein are those of Zurich Insurance Group Ltd as of the date of writing and are subject to change without notice.

This publication has been produced solely for informational purposes. The analysis contained and opinions expressed herein are based on numerous assumptions concerning anticipated results that are inherently subject to significant economic, competitive, and other uncertainties and contingencies. Different assumptions could result in materially different conclusions. All information contained in this publication have been compiled and obtained from sources believed to be reliable and credible but no representation or warranty, express or implied, is made by Zurich Insurance Group Ltd or any of its subsidiaries (the ‘Group’) as to their accuracy or completeness.

Opinions expressed and analyses contained herein might differ from or be contrary to those expressed by other Group functions or contained in other documents of the Group, as a result of using different assumptions and/or criteria.

The Group may buy, sell, cover or otherwise change the nature, form or amount of its investments, including any investments identified in this publication, without further notice for any reason.

This publication is not intended to be legal, underwriting, financial investment or any other type of professional advice. No content in this publication constitutes a recommendation that any particular investment, security, transaction or investment strategy is suitable for any specific person. The content in this publication is not designed to meet any one’s personal situation. The Group hereby disclaims any duty to update any information in this publication.

Persons requiring advice should consult an independent adviser (the Group does not provide investment or personalized advice).

The Group disclaims any and all liability whatsoever resulting from the use of or reliance upon publication. Certain statements in this publication are forward-looking statements, including, but not limited to, statements that are predictions of or indicate future events, trends, plans, developments or objectives. Undue reliance should not be placed on such statements because, by their nature, they are subject to known and unknown risks and uncertainties and can be affected by other factors that could cause actual results, developments and plans and objectives to differ materially from those expressed or implied in the forward-looking statements.

The subject matter of this publication is also not tied to any specific insurance product nor will it ensure coverage under any insurance policy.

This publication may not be reproduced either in whole, or in part, without prior written permission of Zurich Insurance Group Ltd, Mythenquai 2, 8002 Zurich, Switzerland. Neither Zurich Insurance Group Ltd nor any of its subsidiaries accept liability for any loss arising from the use or distribution of publication. This publication is for distribution only under such circumstances as may be permitted by applicable law and regulations. This publication does not constitute an offer or an invitation for the sale or purchase of securities in any jurisdiction.