- In France, Emmanuel Macron is re- elected as French President, defeating right-wing candidate Marine Le Pen

The result represents a continuation of current policies and less uncertainty for investors but the French economy still faces considerable challenges such as the cost of living crisis

- US Fed members present a united front on the need to quicken the pace of tightening

We agree that there is an opportunity to raise the size of rate hikes to 50bps at the next two FOMC meetings, but caution that the back end of the year will see growth slowing appreciably, requiring a gentle touch from the Fed

- China's lockdowns have an increasingly negative impact on logistics and supply chains

We suspect that the slowdown in Chinese growth has accelerated in April and may extend into May

Weekly Market Update

Investments

| Article

| 25 Apr 2022

|

Weekly Macro & Markets View

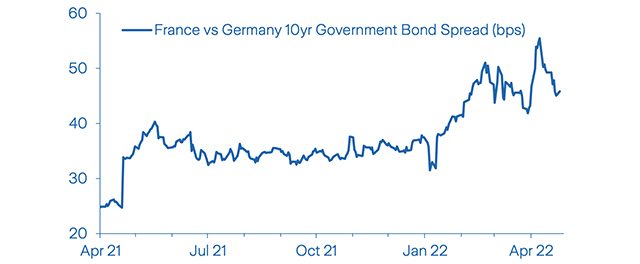

Emmanuel Macron wins historic second term as French President

Source: Bloomberg

Incumbent French President, Emmanuel Macron, has won a second term, the first time for a French President since Jacques Chirac in 2002. In the end Macron won by a comfortable margin, around 58% to Marine Le Pen’s 42%. Investors are likely to react positively to the result, which represents less uncertainty and a continuation of current policies. The initial market reaction has seen French government bond spreads relative to Germany narrowing this morning. Indeed, Macron will likely continue with his policy of gradually liberalising the French economy (e.g. by improving labour market flexibility, reducing corporate taxes and increasing the retirement age) while also promoting digitalisation and the green transition. Nevertheless, the French economy will still face substantial challenges and Macron may be able to do less in terms of reforms than in his first five years as President if his party, En Marche, does not win a parliamentary majority in legislative elections in June. Meanwhile, the latest S&P Flash PMI indices for the Eurozone showed a pickup in services confidence, to 57.7 in April from 55.6 in March, and only a small decline in manufacturing confidence. The data are encouraging as they are some of the first to reflect early Q2 activity. However, risks remain substantial, with the Bundesbank estimating last week that if the Russian gas supply to Germany is cut off it would cause a 5% hit to GDP pushing Germany (and the rest of the Eurozone) into recession.

US: Fed members unsettle markets with hawkish alignment

Another difficult week for investors, with equity and bond markets selling-off as Fed members ramped up hawkish messaging. Data were light, with housing numbers confirming that, while housing starts rose to levels last seen in 2006, there remains a shortage of homes for sale. More notable were the PMI indices. Manufacturing remained strong at 59.7, while services ticked lower to 54.7. However, input and output prices rose to record levels for both series. This implies that companies have pricing power and that inflationary pressures are still rising. Fed members, including Chair Powell, used a number of engagements last week to stress the need to ramp up the pace of rate hikes. As we expected, it now seems a given that a 50bp hike will be forthcoming in May, with perhaps another 50bps in June, as ‘front loading’ the cycle was a key message. While futures pricing is aligned with Fed members’ rhetoric of getting to a neutral rate by year end, the commentary did impact asset prices. 10yr Treasury yields surged once again, closing the week at 2.9%, while the S&P 500 fell 2.75%.

North Asia: China is hit by massive supply chain constraints, while Japan’s deflation ends

March was likely the last month for some time showing deflation in Japan. Core CPI (excluding fresh food and energy) came in at -0.7%, while the headline CPI inched 30bps higher to 1.2%. As of next month the somewhat artificial base effect of the administrative cut to mobile phone charges from a year ago will be out of the way, and we expect core CPI to turn positive and headline CPI to move towards 2%. Meanwhile, Japan’s Manufacturing PMI index ticked lower to 53.4, due to renewed supply chain problems in the auto sector, while the Services PMI climbed back above the boom/bust line of 50, to 50.5, following stabilisation on the Omicron front. In South Korea, following an impressive surge since the Covid-lows of 2020, data for the first twenty days of April suggest exports may be topping out. In China, following a slump in consumption, the ongoing lockdowns, particularly in Shanghai, are negatively affecting industrial production even in less-affected provinces due to massive supply chain issues.

ASEAN: Bank Indonesia holds the policy rate steady, but cuts its GDP forecast

As widely expected, Bank Indonesia maintained its policy rate at 3.5% to preserve currency stability and contain inflation, while supporting the economic recovery. However, it downgraded its GDP growth forecast for the first time this year by 20bps to 4.5-5.3% due to slower global growth and weaker domestic demand amid higher energy and food prices. More positively, Indonesia’s trade surplus climbed to a record high in March, as prices of key exports including coal, palm oil, nickel and steel surged as a result of the Russia-Ukraine war. The higher commodity prices also led Bank Indonesia to raise its 2022 current account balance forecast to a narrower deficit of 0.5-1.3% of GDP (from 1.1-1.9%). Similarly in Malaysia, the trade surplus widened in March, supported by strong export growth in manufacturing, agriculture and mining. Malaysia also reported March headline inflation of 2.2%, while core inflation hit 2.0% for the first time since August 2019, but is still at the low end of Bank Negara Malaysia’s 2022 forecast range of 2-3%.

Australia: Bond yields increase following RBA minutes

As mentioned last week, the RBA minutes were more hawkish than the market expected, increasing the prospect of a 40bp rate hike for June instead of 15bps. The most crucial change in the minutes is the focus on the increase in global inflation and other central bank actions. Previously, the focus was on domestic inflation and the economic outlook. The RBA has shifted away from the view that Australia's inflation outlook is different from the rest of the world. It now acknowledges the increasing risks of global inflation, and that domestic monetary policy needs to be more in line with trends globally. Bond yields increased in reaction to the RBA minutes and the more hawkish comments from the US Fed Chair during the week. The three-year government bond yield rose by 32bps to 2.69%, and the curve flattened for the week. The underlying economic data for Australia remain positive, with the Services PMI index for April rising one point to 56.6 and the Manufacturing PMI index up slightly to 57.9, having maintained a position above 50 since June 2020.

LatAm: Argentina complied with the IMF primary deficit target in Q1

Q1 fiscal revenues and expenditures in Argentina increased 9% and 12% YoY respectively in real terms. The primary fiscal deficit reached ARS 192.7bn, below the ARS 222bn ceiling set in the IMF program. However, March’s fiscal results improved significantly, helped by a surprisingly strong increase in property rents, adding ARS 123.6bn to total revenues. The government did not provide any details to explain the scale of the improvement, which seems to be attributed to an accounting adjustment as the government has systematically issued debt above par, which boosts fiscal revenues. Taking this into account, there appears to have been a deterioration in the fiscal revenues, and the government would have failed to meet the fiscal target. The equity market in LatAm is losing momentum. The MSCI LatAm fell 4.8% during the last week, mainly explained by Brazil. The BRL depreciated 3.8% on Friday, the worst day in nearly two years, driven by diverging speeches from central bankers, with a more hawkish US Fed, while the BCB is close to the end of the hiking cycle.

What to Watch

- In a quiet week for US data, most attention will be on Durable Goods Orders, which are expected to show improvement in March on the weak February readings, while the Conference Board measure of consumer confidence is also expected to tick higher.

- In the Eurozone, further April business and consumer confidence data and the first estimate of Q1 GDP will give an important indication as to the state of the economy.

- We believe the Bank of Japan will keep policy unchanged, while several important economic indicators for March will be released. China will publish both its April NBS and Caixin PMIs on Saturday. A number of markets will be closed on Friday and into the following week.

- In Mexico, Q1 GDP and other key activity indicators will be released. In Chile, the focus will be on unemployment, industrial production, and retail sales.

Disclaimer and cautionary statement

This publication has been prepared by Zurich Insurance Group Ltd and the opinions expressed therein are those of Zurich Insurance Group Ltd as of the date of writing and are subject to change without notice.

This publication has been produced solely for informational purposes. The analysis contained and opinions expressed herein are based on numerous assumptions concerning anticipated results that are inherently subject to significant economic, competitive, and other uncertainties and contingencies. Different assumptions could result in materially different conclusions. All information contained in this publication have been compiled and obtained from sources believed to be reliable and credible but no representation or warranty, express or implied, is made by Zurich Insurance Group Ltd or any of its subsidiaries (the ‘Group’) as to their accuracy or completeness.

Opinions expressed and analyses contained herein might differ from or be contrary to those expressed by other Group functions or contained in other documents of the Group, as a result of using different assumptions and/or criteria.

The Group may buy, sell, cover or otherwise change the nature, form or amount of its investments, including any investments identified in this publication, without further notice for any reason.

This publication is not intended to be legal, underwriting, financial investment or any other type of professional advice. No content in this publication constitutes a recommendation that any particular investment, security, transaction or investment strategy is suitable for any specific person. The content in this publication is not designed to meet any one’s personal situation. The Group hereby disclaims any duty to update any information in this publication.

Persons requiring advice should consult an independent adviser (the Group does not provide investment or personalized advice).

The Group disclaims any and all liability whatsoever resulting from the use of or reliance upon publication. Certain statements in this publication are forward-looking statements, including, but not limited to, statements that are predictions of or indicate future events, trends, plans, developments or objectives. Undue reliance should not be placed on such statements because, by their nature, they are subject to known and unknown risks and uncertainties and can be affected by other factors that could cause actual results, developments and plans and objectives to differ materially from those expressed or implied in the forward-looking statements.

The subject matter of this publication is also not tied to any specific insurance product nor will it ensure coverage under any insurance policy.

This publication may not be reproduced either in whole, or in part, without prior written permission of Zurich Insurance Group Ltd, Mythenquai 2, 8002 Zurich, Switzerland. Neither Zurich Insurance Group Ltd nor any of its subsidiaries accept liability for any loss arising from the use or distribution of publication. This publication is for distribution only under such circumstances as may be permitted by applicable law and regulations. This publication does not constitute an offer or an invitation for the sale or purchase of securities in any jurisdiction.