- The seventh consecutive down week for the S&P 500 now marks the worst streak since 2001

We are encouraged that the S&P 500 bounced off important technical support levels in late Friday trading.

- In Australia the moderate Labor Party has defeated the incumbent and fiscally conservative coalition

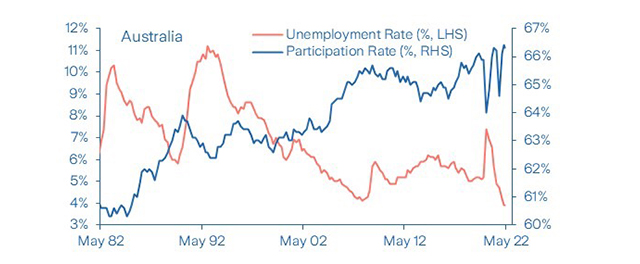

Hawkish RBA minutes and a fall in the unemployment rate to a record low of 3.9% in April drive our expectations for a 40bp policy rate hike for June.

- In the UK both the unemployment rate and consumer confidence fall to the lowest since 1974

Soaring inflation weighs on consumer confidence though household spending is holding up, supported by a very strong labour market.

Weekly Market Update

Investments

| Article

| 23 May 2022

|

Weekly Macro & Markets View

Election outcome and a tight labour market suggest a policy rate hike

Source: Australian Bureau of Statistics, Bloomberg

In Australia, the moderate left Labor Party has defeated the incumbent conservative coalition government, but it is too early to determine if they can form a government outright or will need to form a coalition with the Greens or independents. Independent members received record high votes, supported by fiscal conservative and environmentally progressive voters.

Though the Labor Party’s taxation policy does not differ materially from that of the coalition government, they intend to increase spending on childcare, aged care, and Medicare. These changes will result in slightly further increased pressure on the RBA to normalise monetary policy as the unemployment rate has declined to a historic low of 3.9% while the participation rate stands at the elevated level of 66.3%. The RBA minutes for May highlight concern over further inflation from higher labour costs and the need to normalise monetary policy. The minutes also pointed to a number of risks to the current inflation forecast, especially regarding uncertainty over the timing as to when supply issues can be resolved. In this environment, we expect the RBA will increase rates by 40bps to 0.75% at the June meeting as it would be prudent to front-load rate hikes in this cycle of monetary tightening.

North Asia: China loosens monetary policy, Japan’s Reuters Tankan reveals a mixed picture

China’s PBoC announced a surprising 15bp cut in the 5yr loan prime rate (LPR), a benchmark for mortgage rates, while keeping the 1yr LPR unchanged. Earlier last week the PBoC lowered the floor rate of first home mortgages to 20bps below benchmark, following very weak housing market data for April. In Japan, Q1 GDP contracted slightly. Private consumption held in better than expected, while higher imports contributed to a drag from net exports. The manufacturing component of the Reuters Tankan for May fell to the lowest level in more than a year on elevated input costs and supply chain problems, while the non-manufacturing component improved, rising above pre-pandemic levels. April export volumes contracted on a sequential basis, mainly hit by collapsing trade with China. In South Korea, export data for the first twenty days of May seem brisk, but on a working day adjusted basis trade actually slowed for the second month in a row, which confirms that Asian export strength is rolling over.

ASEAN: Resilient trade surplus region wide, Indonesia lifts palm oil export ban

Malaysia’s April trade surplus narrowed slightly while Indonesia’s widened to a new record high as prices of key commodities exports surged. Looking ahead to May, we expect Indonesia’s palm oil exports to be distorted by the short-lived ban imposed on April 28 and lifted on May 23. We believe more policy changes will be implemented as the price of bulk cooking oil is still far above the IDR 14,000/liter target. Indonesia’s retail sales contracted in April from a year ago, possibly due to higher costs dampening consumer confidence. However, domestic demand likely picked up in May during the Ramadan-Idul Fitri festivities. People mobility to retail and recreation venues rose to nearly 30% above pre-pandemic levels in the first two weeks of May. Given the improving domestic demand and weakening Rupiah, we expect Bank Indonesia to deliver its first 25bp rate hike during the upcoming meeting on May 24. The central banks in both Malaysia and the Philippines have initiated the tightening cycle in the past week.

UK: The unemployment rate and consumer confidence fall to the lowest since 1974

Inflation rates accelerated further in April with headline CPI inflation reaching 9% YoY, which was a tick lower than consensus expectations. The key driver of the latest surge in inflation was the significant jump in energy prices as the regulator Ofgem lifted its price cap by 54%. Core inflation rose less markedly than the headline number from 5.7% YoY the month before to 6.2% YoY, in line with expectations. Rising living costs continue to weigh on households’ minds with the consumer confidence index falling to the lowest level since records began in 1974, reflecting the real income squeeze and an increasingly uncertain growth outlook. So far, however, household spending is holding up well despite depressed consumer confidence. Retail sales rose 1.4% MoM in April. Spending is supported by a very strong labour market. The unemployment rate ticked down to 3.7% in March, the lowest level since 1974. Fueled by the tight labour market, wage growth (excluding bonuses) ticked up from 4.1% in February to 4.2% YoY.

LatAm: A faster than expected deceleration in Chile

In Chile, Q1 GDP grew 7.2% YoY, well below the 7.9% implied by the preliminary monthly economic figures. On a quarterly basis, GDP contracted by 0.8% QoQ. Fixed investment was the main driver of the contraction, falling 5.9% QoQ, with all its components showing a contraction. Fixed investment should continue to fall, considering the uncertainty of the constitutional process. Private consumption fell by 0.3% QoQ, mainly explained by the contraction in non-durable goods, while government consumption expanded by 6.3% QoQ.

Private consumption will likely continue to adjust to the downside after the excessive stimulus deployed in 2021 and the higher inflation impacting real purchasing power. We expect domestic demand will continue to fall, leading the economy into a technical recession in Q2. In Brazil, the Audit Court authorised the privatisation of Electrobras, which generates ~30% of all electricity in the country. The government seeks to raise BRL 67bn with the privatisation, which is expected to happen before the October presidential election.

Credit: High Yield vulnerability gains visibility

Credit markets were volatile again last week. Both cash and CDS spreads tightened on Tuesday as investors interpreted Fed Chair Powell’s comments positively. However, the mood soured on Wednesday, following weak guidance by the US retailer Target. The S&P 500 dropped 4% and the USD IG CDS Index widened 7bps to surpass 90bps, a level not seen since May 2020. Poor sentiment was also visible in fund flows. According to Lipper, USD IG funds saw their eighth straight week of outflows, with withdrawals of USD 4.27bn, following over USD 8bn the prior week. The fund flow dynamics for leveraged loans has also changed. After a long stretch of inflows, loan funds saw outflows of USD 1.57bn, the largest since March 2020. Notably, High Yield has finally begun to underperform Investment Grade, especially in the US, where the HY/IG spread ratio decompressed. While the ratio was at historically low levels it remains low compared to the historical average, confirming our view that risk reward in High Yield seems skewed to the downside, especially in the event of a recession.

What to Watch

- PMI data for the major economies are expected to show a further modest slowdown in growth in May.

- In the Eurozone, various business confidence surveys, including the German ifo survey, will give important clues as to the state of economic activity in May.

- In APAC, we expect Bank of Korea, Bank Indonesia, and the Reserve Bank New Zealand to lift their policy rates. Tokyo’s May CPI, Taiwan’s Q1 GDP, Hong Kong’s April exports as well as April industrial production data in Singapore and Thailand will be in focus. Indonesia’s markets will be closed on Thursday.

Disclaimer and cautionary statement

This publication has been prepared by Zurich Insurance Group Ltd and the opinions expressed therein are those of Zurich Insurance Group Ltd as of the date of writing and are subject to change without notice.

This publication has been produced solely for informational purposes. The analysis contained and opinions expressed herein are based on numerous assumptions concerning anticipated results that are inherently subject to significant economic, competitive, and other uncertainties and contingencies. Different assumptions could result in materially different conclusions. All information contained in this publication have been compiled and obtained from sources believed to be reliable and credible but no representation or warranty, express or implied, is made by Zurich Insurance Group Ltd or any of its subsidiaries (the ‘Group’) as to their accuracy or completeness.

Opinions expressed and analyses contained herein might differ from or be contrary to those expressed by other Group functions or contained in other documents of the Group, as a result of using different assumptions and/or criteria.

The Group may buy, sell, cover or otherwise change the nature, form or amount of its investments, including any investments identified in this publication, without further notice for any reason.

This publication is not intended to be legal, underwriting, financial investment or any other type of professional advice. No content in this publication constitutes a recommendation that any particular investment, security, transaction or investment strategy is suitable for any specific person. The content in this publication is not designed to meet any one’s personal situation. The Group hereby disclaims any duty to update any information in this publication.

Persons requiring advice should consult an independent adviser (the Group does not provide investment or personalized advice).

The Group disclaims any and all liability whatsoever resulting from the use of or reliance upon publication. Certain statements in this publication are forward-looking statements, including, but not limited to, statements that are predictions of or indicate future events, trends, plans, developments or objectives. Undue reliance should not be placed on such statements because, by their nature, they are subject to known and unknown risks and uncertainties and can be affected by other factors that could cause actual results, developments and plans and objectives to differ materially from those expressed or implied in the forward-looking statements.

The subject matter of this publication is also not tied to any specific insurance product nor will it ensure coverage under any insurance policy.

This publication may not be reproduced either in whole, or in part, without prior written permission of Zurich Insurance Group Ltd, Mythenquai 2, 8002 Zurich, Switzerland. Neither Zurich Insurance Group Ltd nor any of its subsidiaries accept liability for any loss arising from the use or distribution of publication. This publication is for distribution only under such circumstances as may be permitted by applicable law and regulations. This publication does not constitute an offer or an invitation for the sale or purchase of securities in any jurisdiction.