- Inflation hits another record high in the Eurozone, while ECB President Christine Lagarde hints at a rapid end to QE

The ECB is under pressure to address the inflation problem in the Eurozone and is likely to end QE asset purchases quickly and then raise interest rates.

- US Q1 GDP falls while labour costs and home prices surge

GDP is distorted by imports and restocking, with underlying consumption and capital spending robust, which, along with record gains in home prices, supports a hawkish Fed this week.

- Credit markets weaken notably with Europe reaching non-recessionary peak levels

While risks abound, investor pessimism seems somewhat excessive and higher yields should eventually draw liability driven investors as credit fundamentals remain strong.

Weekly Market Update

Investments

| Article

| 02 May 2022

|

Weekly Macro & Markets View

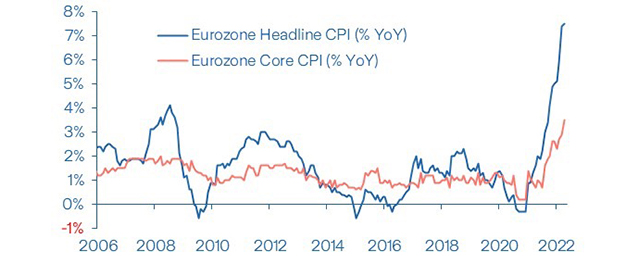

Record high inflation adds to pressure on ECB

Source: Bloomberg

Eurozone inflation hit another record high at 7.5% YoY in April on the headline measure, up from 7.4% in March, while core inflation also picked up to 3.5% from 2.9%. Although the Eurozone economy grew in Q1, the increase in GDP was only 0.2% QoQ. The spike in inflation makes the ECB’s job harder and there was further hawkish rhetoric from policymakers last week including ECB President Christine Lagarde, who said that the ECB would end QE asset purchases early in Q3, ‘probably in July’ and then consider raising interest rates. Financial markets are pricing in a series of rate increases by the ECB beginning in July. We are not quite so hawkish but do expect the ECB deposit rate to reach at least zero by the end of 2022 (it is currently minus 0.5%), and we are expecting the first ECB rate hike in September.

At the moment, most of the spike in headline inflation in the Eurozone is due to non-core components such as oil and food prices. Energy inflation is currently contributing around four percentage points to total inflation and food prices another one percentage point. Both should eventually fall out of the annual comparison. Nevertheless, the rise in core inflation is worrying and points to underlying pricing pressures also increasing. The ECB will be concerned that long-term inflation expectations do not rise too far and that a wage-price spiral does not develop. Hence their caution and Christine Lagarde’s comments last week.

Credit: Notable market weakness with European spreads reaching non-recessionary peaks

Credit markets were notably weaker last week with spreads wider across sectors and geographies. European credit markets bore the brunt of the weakness with spreads now reaching typical non-recessionary peak levels since the Eurozone crisis, implying further weakness would be justified only in case of a recession or another crisis. What is even more noteworthy is that all-in funding costs for companies implied by corporate bond yields have surged to peak Covid crisis levels, this time driven by the rise in government bond yields rather than by credit spreads. Investor angst is evident in the continued outflows from credit funds as well as in muted supply. While risks abound, investor pessimism seems somewhat excessive. Higher yields and credit spreads are likely at some stage to bring in liability driven investments as credit fundamentals remain strong with default rates expected to stay low. Furthermore, we believe that despite the hawkish rhetoric, central banks are likely to be pragmatic and the Fed meeting this week will be keenly watched in this context.

US: Strong economic readings undermine equities

A week of robust economic data, including surging house prices and strong wage growth, support more assertive monetary policy, but proved unnerving for investors, as the tech heavy Nasdaq index plunged 3.9% on the week. The index closed April down 13%, the worst monthly performance since 2008, not helped by the 14% fall in Amazon stock on Friday. The rising rate environment has undermined financial markets this year and until evidence of peaking inflation or a moderation in policy expectations emerge, the road is likely to remain bumpy. As previously noted, this week’s FOMC meeting will be on the hawkish side, with a 50bp hike a near certainty. Q1 GDP came in last week at -1.4% QoQ annualised, but this fall was misleading, driven by massive inventory restocking as real imports of goods rose 20.5% QoQ annualised while consumer and capital spending were strong. House prices are now rising at a record pace of 20.2%YoY, and while the core PCE inflation reading ticked lower to 5.2% YoY in March, the Employment Cost Index rose 1.4% in Q1, to 4.5% YoY.

Switzerland: Consumer sentiment tumbles, but a strong labour market keeps spending on track

The Swiss economy continues to expand at a solid pace, though growth is on a slowing trajectory. The Manufacturing PMI edged lower in April, led by weak current output and a further fall in delivery times, but remains well above the historical average. The Services PMI also fell, following a period with strong pent-up demand for consumer services, but overall activity is still strong. By contrast, consumer sentiment slumped in April, marking the largest decline since the onset of the pandemic. While rising prices and the Ukraine situation are weighing on sentiment, households are positive about the job market, which helps to explain resilient spending. The franc weakened sharply against the dollar last week, but the currency remains highly valued vs the euro and a broad nominal exchange rate index is close to a historical high. We do not expect the SNB to shift its policy guidance in response to the latest currency moves, given the fraught geopolitical outlook and risk of renewed upward pressure on safe-haven assets, including the Swiss franc.

China: Politburo urges acceleration of infrastructure investment to counter economic slump

China’s Politburo, led by President Xi, called for a quick and effective increase in infrastructure investments to counter the collapse of economic activity in major provinces amid the Omicron related lockdowns. The move was applauded by investors and Chinese equities rallied on Friday with the MSCI China up 5.8%, though it is still down 17.2% YTD. China’s economy has been hit by the major lockdowns in Shanghai and other provinces. In the province of Jilin, an auto manufacturing hub neighbouring North Korea and Russia, GDP contracted by 7.9% YoY in Q1, with industrial production down 36.7% YoY in March. The slump is expected to have accelerated in April. Nationwide, the NBS Manufacturing PMI fell 2.1 points to 47.3 in April, while the Caixin Manufacturing PMI fell 2.1 points to 46. In both surveys, the new order and new export order indices contracted significantly. The drop in the NBS Non-Manufacturing PMI was more even severe, down 6.1 points to 41.9, driven by both services and construction.

Japan: JPY weakens to 130 versus USD as the BoJ stands pat

Having started the year at 115, USDJPY rallied above the 130 mark as the Bank of Japan (BoJ) reiterated its commitment to maintaining its low interest rate policy. The BoJ will conduct fixed-rate, unlimited bond buying operations on a daily basis to cap the 10yr yield at 0.25% and will keep the easing bias in the forward guidance of its rates unchanged. We believe that monetary policy will not be changed at least until the July Upper House elections, while Covid related emergency funding will only be phased out after September. The BoJ also cut its median growth forecast from 3.8% to 2.9% for this fiscal year but increased it from 1.1% to 1.9% for next fiscal year. Moving to March activity data, industrial production recovered by 0.3% MoM, driven by machinery and chemicals production, while motor vehicle production fell 6% on renewed supply chain disruptions. March retail sales recovered above their pre-Covid levels in value terms but are still lagging in volume terms. The rebound was driven by auto, household appliance and apparel sales.

What to Watch

- The important US ISM and jobs data this week are likely to be overshadowed by the FOMC meeting, at which a 50bp hike is fully expected, with attention focused on Chair Powell’s testimony and Q&A session.

- In the UK, the Bank of England is expected to raise interest rates by another 25bps this week, while in the Eurozone various economic data will show how strong the recovery is currently.

- In APAC, many markets will be closed for several days or the whole week due to various public holidays and religious festivals. Several Asian countries will release April CPI statistics, while Hong Kong’s Q1 GDP statistics are expected to confirm a contraction. Tokyo’s April CPI is likely to exhibit the end of deflation with statistical base effects out of the way. In Australia, the RBA hiking cycle may start earlier than expected when the MPC convenes on Tuesday.

- We expect inflation to continue accelerating and surpass 10% YoY in Chile. In Brazil, the Central Bank will likely hike the Selic rate by 100bps and provide some forward guidance regarding its next steps.

Disclaimer and cautionary statement

This publication has been prepared by Zurich Insurance Group Ltd and the opinions expressed therein are those of Zurich Insurance Group Ltd as of the date of writing and are subject to change without notice.

This publication has been produced solely for informational purposes. The analysis contained and opinions expressed herein are based on numerous assumptions concerning anticipated results that are inherently subject to significant economic, competitive, and other uncertainties and contingencies. Different assumptions could result in materially different conclusions. All information contained in this publication have been compiled and obtained from sources believed to be reliable and credible but no representation or warranty, express or implied, is made by Zurich Insurance Group Ltd or any of its subsidiaries (the ‘Group’) as to their accuracy or completeness.

Opinions expressed and analyses contained herein might differ from or be contrary to those expressed by other Group functions or contained in other documents of the Group, as a result of using different assumptions and/or criteria.

The Group may buy, sell, cover or otherwise change the nature, form or amount of its investments, including any investments identified in this publication, without further notice for any reason.

This publication is not intended to be legal, underwriting, financial investment or any other type of professional advice. No content in this publication constitutes a recommendation that any particular investment, security, transaction or investment strategy is suitable for any specific person. The content in this publication is not designed to meet any one’s personal situation. The Group hereby disclaims any duty to update any information in this publication.

Persons requiring advice should consult an independent adviser (the Group does not provide investment or personalized advice).

The Group disclaims any and all liability whatsoever resulting from the use of or reliance upon publication. Certain statements in this publication are forward-looking statements, including, but not limited to, statements that are predictions of or indicate future events, trends, plans, developments or objectives. Undue reliance should not be placed on such statements because, by their nature, they are subject to known and unknown risks and uncertainties and can be affected by other factors that could cause actual results, developments and plans and objectives to differ materially from those expressed or implied in the forward-looking statements.

The subject matter of this publication is also not tied to any specific insurance product nor will it ensure coverage under any insurance policy.

This publication may not be reproduced either in whole, or in part, without prior written permission of Zurich Insurance Group Ltd, Mythenquai 2, 8002 Zurich, Switzerland. Neither Zurich Insurance Group Ltd nor any of its subsidiaries accept liability for any loss arising from the use or distribution of publication. This publication is for distribution only under such circumstances as may be permitted by applicable law and regulations. This publication does not constitute an offer or an invitation for the sale or purchase of securities in any jurisdiction.