- Credit markets start the year on a weak note, which is generally considered a poor omen for returns

We don’t expect a bear market for credit in 2022, but upside seems limited, especially versus equities as spreads appear to be tight even after accounting for strong credit fundamentals.

- Stocks slip further in choppy trading, as the buy-on-dip mantra of investors is tested

Though equity markets remain under pressure, key support levels are close, while the start of the earnings season has the potential to rejuvenate investor sentiment and keep the long-term uptrend in place.

- US headline inflation has accelerated to 7% YoY, the highest since 1982

High inflation weighs on households’ minds, but there are increasing signs that price pressure is abating including weaker PPI measures, falling import prices and a tick down in price plans.

Weekly Market Update

Investments

| Article

| 17 Jan 2022

|

Weekly Macro & Markets View

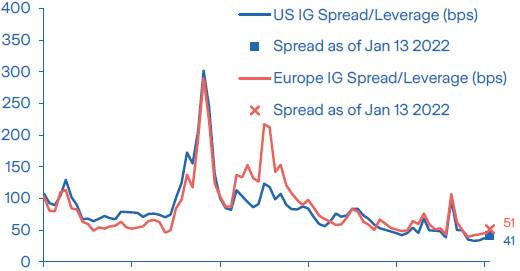

Limited upside in credit

Source: Bloomberg

Negative performance in credit at the beginning of the year is generally considered to forebode poor returns for the year. Last week saw spreads continuing to soften especially in investment grade credit. While corporate bonds were resilient at the beginning of the year compared to derivatives, they notably underperformed last week. Primary markets are also showing signs of weakness. Although issuance volumes have been strong in both US and European investment grade markets, investor demand seems to be weakening. Many debt deals have come with hefty new issue concessions, while oversubscription levels have been lacklustre. Last but not least, flows seem to be flat lining since late last year as technicals weaken due to volatility in bond yields and expected tightening by central banks. High yield spreads have fared better so far this year than investment grade, likely driven by higher energy prices and lower sensitivity to bond yields. That said, given negative fund flows in high yield seen last week, this outperformance may soon ebb.

While we don’t expect a bear market for credit in 2022, it seems that further upside, especially relative to equities seems limited. Fundamentals should remain strong in the near term, but as shown in the chart, spreads are already pricing this in.

US: Inflation rises to the highest in four decades

Headline CPI inflation ticked up to 7% YoY in December from 6.8% the month before. Although this is the highest level since 1982 there are increasing signs that inflation rates are about to peak. Producer price increases slowed to 0.2% MoM from 1.0% in November and import prices even fell by 0.2% MoM. Further on, small businesses’ price plans, which have soared recently, ticked down in December as well. Though inflation will remain high in the very near term we expect rates to fall markedly over the course of the year. Falling inflation would help to support consumer sentiment, which has deteriorated slightly in January according to the University of Michigan’s recent survey. Reflecting households’ less optimistic stance, retail sales fell by a substantial 1.9% MoM in December, dragged down by a decrease in online sales. While this number is weaker than expected it has to be put into context with strong growth back in October, indicating that households brought forward their Christmas shopping due to potential supply chain concerns.

Eurozone: Downside risks to German Q4 GDP implied by full-year growth estimate

Last week the German statistics office issued an estimate of 2.7% YoY full-year growth for 2021. This estimate usually comes out before the estimate for QoQ growth for Q4, implying that QoQ growth in 2021 Q4 in Germany was probably negative. The official figure will be released at the end of the month. The upshot is that downside risks to the German and Eurozone Q4 GDP figure have increased. However, investors will likely look through this as economic conditions for 2022 still look bright. The Eurozone economy seems to be coping reasonably well with the Omicron surge. Even supply-chain problems in the auto sector appear to be easing, with the latest Eurozone industrial production data showing a second large consecutive jump in motor vehicle production. Meanwhile, political uncertainty continues in Italy ahead of the January 24 presidential elections, with Silvio Berlusconi saying that his party, Forza Italia, would pull out of the government coalition if Draghi is elected as President. This could then precipitate snap elections.

China: The PBoC cuts policy rates by 10bps amid risks to consumption and housing

China’s GDP was up 8.1% last year, roughly in line with our forecast and better than forecasts by several major brokers. Stronger growth momentum in Q4 was boosted mainly by solid industrial production and manufacturing investment following a strong export performance. Infrastructure investment also contributed positively. On the other side of the coin, we note a slowdown in private consumption and property investment. The recent Omicron related lockdowns in major cities like Xian, Tianjin and Anyang as well as the request by authorities to avoid travelling and visiting relatives during the upcoming Lunar New Year holidays suggest that retail sales and particularly services consumption will suffer in Q1. Though policy loosening is expected to gain speed, as evidenced by today’s 10bps cut in two policy rates to a record low, it will take until later this year to have a positive impact on housing demand. While headwinds are severe, we think the fact that this year is decisive politicaly will urge the government to spur economic growth.

LatAm: Positive surprises in services and retail sales in Brazil, while core inflation accelerates

The MSCI LatAm outperformed other emerging markets, rising 5%, with Chile increasing 7%. In Chile, the President-elect delivered a balanced speech to business leaders, mentioning that fiscal responsibility is important. The Lower House approved a bill for financing a universal pension for the most vulnerable 90% population, eliminating tax exemptions to boost revenues and incorporating a new wealth tax requested by the opposition deputies. The Finance Minister said that the latter is unconstitutional, as only the President can propose tax changes. The Government will wait until the Senate discusses the bill before taking the matter to the Constitutional Court. In Brazil, headline inflation increased 0.73% MoM in December and annual inflation ended 2021 at 10.1%. Core prices accelerated, closing 2021 at 7.4%. Service output jumped 2.4% MoM in November, showing widespread improvement. After declining for three consecutive months, retail sales for November were stronger than expected, rising 0.5% MoM.

Covered Bonds: Off to a strong start in 2022

Despite an impressive surge in new issuance, covered bond spreads remained unscathed by the recent market volatility. Covered bonds strongly outperformed other credit markets segments and ended the week with only a modest 1bps widening. Following the rebound in early December, the primary market took off with several well-established large issuers from Germany, Austria and France coming back to the market. We believe this trend will continue and gross issuance volume is expected to significantly rebound versus 2021. However, net supply should remain negative as refinancing needs stand at EUR 136bn in 2022, with January alone seeing a hefty EUR 33bn in redemptions. Moreover, the ECB will likely reinvest EUR 10bn in its Asset Purchase Programme, providing strong support to the market. Another tailwind for covered bonds should come from the recent rise in government bond yields. None of this year’s covered bonds have been issued with a negative yield, which should broaden demand from a wider investor base.

What to Watch

- In the Eurozone, the ZEW survey and inflation data will provide further information on the outlook for the economy.

- We expect the central banks of Japan, Malaysia, and Indonesia to stand pat this week. Several Asian countries will release export data for December. Australia’s labour data for December should remain buoyant given a robust recovery in activity.

Disclaimer and cautionary statement

This publication has been prepared by Zurich Insurance Group Ltd and the opinions expressed therein are those of Zurich Insurance Group Ltd as of the date of writing and are subject to change without notice.

This publication has been produced solely for informational purposes. The analysis contained and opinions expressed herein are based on numerous assumptions concerning anticipated results that are inherently subject to significant economic, competitive, and other uncertainties and contingencies. Different assumptions could result in materially different conclusions. All information contained in this publication have been compiled and obtained from sources believed to be reliable and credible but no representation or warranty, express or implied, is made by Zurich Insurance Group Ltd or any of its subsidiaries (the ‘Group’) as to their accuracy or completeness.

Opinions expressed and analyses contained herein might differ from or be contrary to those expressed by other Group functions or contained in other documents of the Group, as a result of using different assumptions and/or criteria.

The Group may buy, sell, cover or otherwise change the nature, form or amount of its investments, including any investments identified in this publication, without further notice for any reason.

This publication is not intended to be legal, underwriting, financial investment or any other type of professional advice. No content in this publication constitutes a recommendation that any particular investment, security, transaction or investment strategy is suitable for any specific person. The content in this publication is not designed to meet any one’s personal situation. The Group hereby disclaims any duty to update any information in this publication.

Persons requiring advice should consult an independent adviser (the Group does not provide investment or personalized advice).

The Group disclaims any and all liability whatsoever resulting from the use of or reliance upon publication. Certain statements in this publication are forward-looking statements, including, but not limited to, statements that are predictions of or indicate future events, trends, plans, developments or objectives. Undue reliance should not be placed on such statements because, by their nature, they are subject to known and unknown risks and uncertainties and can be affected by other factors that could cause actual results, developments and plans and objectives to differ materially from those expressed or implied in the forward-looking statements.

The subject matter of this publication is also not tied to any specific insurance product nor will it ensure coverage under any insurance policy.

This publication may not be reproduced either in whole, or in part, without prior written permission of Zurich Insurance Group Ltd, Mythenquai 2, 8002 Zurich, Switzerland. Neither Zurich Insurance Group Ltd nor any of its subsidiaries accept liability for any loss arising from the use or distribution of publication. This publication is for distribution only under such circumstances as may be permitted by applicable law and regulations. This publication does not constitute an offer or an invitation for the sale or purchase of securities in any jurisdiction.