Source: Bloomberg

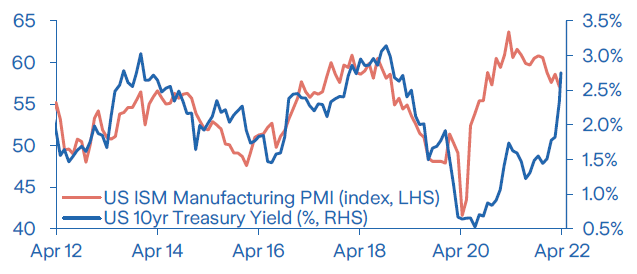

Despite a challenging economic backdrop, with Covid disruptions in Asia, weakening US consumer sentiment and an energy crunch in Europe, government bond yields rose further last week. In Europe, the 10yr Bund yield breached 0.7% for the first time since 2018, ahead of this week’s ECB meeting. In the US, the Fed published the minutes from the March meeting. They were broadly in line with expectations but led to a repricing at the long end of the Treasury curve as focus shifted towards the Fed’s plans for quantitative tightening (QT). This was most notable in the 5yr5yr forward rate, which surged by 46bps. At close to 2.7%, up from 2% in early March, pricing now better reflects the economic fundamentals. Longer maturity yields spiked, with the 10yr and 30yr yields both approaching 2.75% for the first time since early 2019, allowing the 2/10 yield spread, which is a widely watched recession indicator, to turn positive again. While this is encouraging, last week’s rise in yields mainly reflected higher real yields as inflation expectations stabilised, despite surging energy costs, and there was further passthrough to US mortgage rates, which have risen to a decade high. Tighter financial conditions will have an impact on economic activity, and we suspect the growth outlook will increasingly come into focus, also for bond investors.

US: Higher yields weigh on technology stocks

The S&P 500 fell by 1.3% last week as further hawkish comments from individual Fed members drove longer-term Treasury yields to the highest in more than three years. Higher yields weighed on technology stocks in particular with the Nasdaq shedding almost 6% from peak to trough before ending the week close to the intra-week lows with a loss of 3.9%. According to the Fed minutes that were published last week, the balance sheet reduction is expected to begin in May with a few months of ramp up to a maximum monthly pace of USD 60bn for Treasuries and USD 35bn for MBS, which is largely in line with expectations. The minutes also indicate that the FOMC would probably have hiked the fed funds target rate by 50bps in March had the war in Ukraine not increased uncertainty around the time of the meeting. Not a lot of economic data were published last week but the ISM Services Index reaccelerated to 58.3 with both new orders and employment picking up, reflecting ongoing strength in the service sector.

Eurozone: Hard data holding up better than sentiment surveys so far

Despite some plummeting business and consumer confidence surveys recently, so called ‘hard data’ of actual economic activity are holding up better. For instance, Eurozone retail sales rose 0.3% MoM (5.0% YoY) in February. German industrial production also grew in February, though the number was flattered by a large contribution from the volatile energy component. Even if the hard data were weaker in March, the Eurozone is still likely to have grown at a decent pace in Q1. Meanwhile, we are getting initial news on the wage-bargaining negotiations in Germany. The chemical workers union employers agreed to a one-off EUR 1,400 payment to workers in 2022, with a further review of wages pushed back to September. This represents a pay increase of around 4-5%, higher than in recent years, but not the full increase in headline inflation. Finally, as expected, Emmanuel Macron and Marine Le Pen made it through to the second round of the French presidential elections. Opinion polls suggest Macron is the favourite to win, but the gap in the opinion polls between the two candidates has narrowed considerably.

North Asia: Lockdowns hit consumption and cause supply chain disruptions in China

Chinese stocks fell further today as Omicron cases continue to surge in Shanghai despite the severe lockdown that is causing some discontent among the public. There are also fears that a lockdown may be imminent in Guangzhou, the capital of Guangdong province adjacent to Hong Kong. Meanwhile, the Caixin Services PMI for March plunged from 50.2 to 42 in March, reflecting the impact of lockdowns and mobility restrictions in several provinces. Today’s inflation data for March show that the PPI-CPI gap has narrowed from 7.9 to 6.7 ppts, while credit data for March were solid and suggest monetary easing. In Japan, the Eco Watchers survey for March reveals that the outlook for households is improving, which stands in stark contrast to the deteriorating consumer confidence survey for the same month. We suspect that the end of Omicron related restrictions is driving the former, while concerns about higher inflation is driving the latter. Wages improved in February, but real wages remain near zero due to rising inflation.

Australia: The RBA removes the word ‘patient’ from monetary policy, setting up a June rate hike

While the RBA kept rates on hold at the April meeting the post-meeting statement was more hawkish than the market had anticipated. The bank acknowledged increasing wage growth pressure for certain sectors and dropped the reference to being prepared to be ‘patient’ in monitoring inflation. We expect they will commence interest rate hikes to prevent higher inflation expectations from becoming anchored, initiating the first rate hike since November 2010. The Financial Stability Review released by the RBA highlighted the risk of loan performance deterioration from the higher interest risk of increased living costs. While lending standards have generally been strong in Australia, the RBA pointed to an increase in the number of higher debt-to-income loans as an area of concern. In trade data, a sharp 12.1% increase in imports for February narrowed the trade surplus to AUD 7.5bn from AUD 11.8bn. The growth in imports, consumption and intermediate goods highlights considerable economic momentum in the recovery from the surge in Omicron lockdowns.

US ABS: Record issuance met strong investor demand

Issuance activity for US ABS remained brisk and Q1 volume was the highest first quarter issuance since 2007. We expect this strong momentum to continue as consumers seem increasingly willing to borrow. The latest data released by the Fed confirmed a surge in consumer credit with credit card balances rising at an impressive 20.7% annualised rate in February. This should support issuance given lenders’ appetite to fund their balance sheet through the ABS market. Despite this higher supply, final pricing spreads continue to come inside guidance and oversubscription levels remain robust. ABS spreads have outperformed other credit sectors YTD and we expect this trend to continue given benign performances. Delinquencies and losses continue to normalise and remain in line or below pre-pandemic levels. In the Student Loan space, the Department of Education has extended the current payment moratorium through the end of August. This should support households at a time when rising inflation is affecting disposable income.