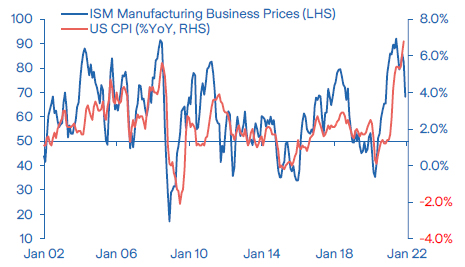

- ISM manufacturing business pricesfall to the lowest in more than a year

The significant drop in manufacturing prices indicates that inflation rates are likely to fall markedly this year.

- Stocks and bonds falter as sticky inflation and more hawkish pricing of central bank policy unsettles investors

Bond moves were aggressive and partly technical in nature, while growth and tech stocks felt pressure from rising discount rates. Volatility will remain a feature, but moves should not be extrapolated.

- Loan repayment issues continue to plague Chinese property companies

We believe policy support intended to revive housing demand is starting to become effective.

Weekly Market Update

Investments

| Article

| 10 Jan 2022

|

Weekly Macro & Markets View

Slowing price pressure points to falling inflation in 2022

Source: Bloomberg

Though receding from their levels a month ago in December, both the ISM Manufacturing Index as well as the ISM Services Index are still reflecting strong growth momentum in the US. In addition, there are more and more signs that price pressure is starting to abate. The ISM Manufacturing’s Report on Business Prices, which has been a good indicator for changing trends in inflation in the past, fell to its lowest level since November 2020. We expect headline inflation to slow markedly over the course of the year as supply chain disruptions should continue to be resolved and base effects are kicking in. Meanwhile, the employment situation improved further in December. Although the number of new payrolls was below expectations (particularly as they have been revised up significantly for the two months before) the unemployment rate dropped to 3.9% from 4.2% in November ⎯ not far from prepandemic levels. While the general economic environment remains supportive for stocks, investors were spooked by the FOMC’s hawkish tone in the latest Fed minutes. An earlier end of the tapering process and a number of expected rate hikes in 2022 were well digested by the market, but the potential for an accelerated balance sheet reduction injects new uncertainty and is likely to lead to more volatile markets this year.

Markets: Bonds and equities take a hit as investors reappraise Fed actions

US data and Fed minutes spooked investors last week, with bond yields surging and stocks coming under pressure. While we do think volatility will be a defining characteristic of 2022, we are more upbeat on the overall direction for stocks. That noted, with higher rates and the Fed’s balance sheet potentially shrinking faster than expected, the start ofthe year has already been challenging. The tech heavy Nasdaq fell 4.5%, with Apple momentarily hitting a record USD 3tn market cap on Tuesday before big tech also came under pressure. With the MSCI World Index off 1.7%, the UK FTSE100 was one of the few markets to post positive gains, following a number of years of disappointing performance. Bonds were also under fire based on still disturbing inflation prints and shifting sentiment on rates. While 10yr Treasuries surpassed March highs to close at 1.76%, Europe also saw a similar move, with the Swiss 10yr back in positive territory for the first time since 2018.

Eurozone: Services sentiment weakens, inflation touches another record high

The final Eurozone Composite PMI was virtually unchanged from the flash estimate, at 53.3 in December, down from 55.4 in November. The fall was mainly due to a lower services PMI, 53.1 in December down from 55.9 in November, due to Omicron news and increased restrictions, while manufacturing confidence remained strong. Overall, the survey suggests that growth in the region slowed around the turn of the year, but is maintaining a decent pace. Meanwhile, Eurozone headline inflation was stronger than expected in December, rising a further tenth of a percentage point to 5.0% YoY from 4.9% in November, while core inflation was unchanged at 2.6%. Although energy and services inflation fell, non-energy industrial goods inflation rose. We expectthat inflation will fall back early this year, especially with the German VAT hike fallingout of the annual comparison, but headline inflation will likely remain above the ECB’s target for most, if not all, of this year.

Asian PMIs: A mixed bag, but overall still robust

Asian headline Manufacturing PMIs moderated, but remain at a healthy level, which is exemplified by India and Indonesia. Both PMIs contracted, but from a high level. The exception is Thailand’s PMI, which contacted below the boom-bust line of 50. It is encouraging that Vietnam’s PMI keeps creeping higher despite the difficult Covid environment. Taiwan’s Manufacturing PMI remains brisk at 55.5, with relevant sub-indicators improving markedly, suggesting that supply chain issues are abating. Export momentum remains solid. In South Korea, both the output and new export order components reveal some weakness. Export growth is already slowing, though vessel exports may be distorting the statistics. At first glance, China’s economy seems to be recovering as both the NBS and Caixin PMIs advanced further above the 50 boom/busline. However, small companies continue to struggle, and the weak new order and employment subcomponent of the NBS Non-manufacturing PMI suggest that challenges remain.

China: Policy support should help to spur housingdemand

China’s ailing property sector reveals a mixed picture. Following last year’s default by Evergrande and Kaisa on overseas listed bonds, Shimao Property failed to repay aloan due to liquidity constraints last week. Shimao’s bonds and equity prices tumbled on Friday but bounced back today. Overall, Hong Kong listed property heavyweight shave rallied recently on policy support by China’s authorities. While avoiding direct assistance to ailing property companies on moral hazard concerns, the government has implemented measures to spur housing demand by easing financing restrictions. Potential home buyers will have easier and cheaper access to mortgages, while banksare encouraged to extend loans to property companies. The next four months will be critical as the loan repayment schedule is challenging, with more company failures expected. However, we believe that policy easing will encourage home buyers to apply for mortgages and that housing demand will slowly recover and then gain traction into the second half of 2022.

LatAm: The central bank of Argentina (BCRA) raisesthe policy rate amid IMF negotiations

In Argentina, the BCRA hiked the benchmark rate (28-day Leliq rate) by 200bps to 40%. They also implemented some changes to its policy framework, adding a new 180-day Leliq instrument, aiming to extend the central bank’s remunerated liability maturities. While helpful, these measures are not enough to adjust the macro economic imbalances in regard to the fiscal path required by the IMFto reach an agreement on the stand-by facility. Considering the low net reserves, which only cover a couple of additional months of public debt payments, we expect a deal with the IMF in March. Headline inflation in Mexico and Chile reached 7.4% and 7.2% respectively in 2021, both above target, and continues to pressure the monetary authorities to tighten. In Brazil, industrial production declined 0.2% MoM in November, suggesting a downside risk for the Q4 2021 GDP. The drop was driven by capital goods production, partially offset by a recovery in the auto sector and durable goods production.

What to Watch

- In the US, investors will focus on the latest set of inflation data while retail sales numbers and consumer confidence will provide insights into the current state of US households.

- Japan’s Eco Watcher survey for December is expected to remain roughly stable in solid territory, while December wholesale prices are likely to have increased to the highest level since 1985. China will report December statistics for foreign trade, money supply and credit as well as CPI and WPI. India’s foreign trade data for November and December CPI will be reported. It is highly likely that the Bank of Korea will lift its policy rate by 25 bps again either this week or in February.

- In Brazil, the focus will be on inflation for 2021 and retail sales for November, which may add additional downside risk to Q4 GDP. In Mexico, November’s industrial production will be published, while in Argentina, we expect inflation to accelerate in December.

Disclaimer and cautionary statement

This publication has been prepared by Zurich Insurance Group Ltd and the opinions expressed therein are those of Zurich Insurance Group Ltd as of the date of writing and are subject to change without notice.

This publication has been produced solely for informational purposes. The analysis contained and opinions expressed herein are based on numerous assumptions concerning anticipated results that are inherently subject to significant economic, competitive, and other uncertainties and contingencies. Different assumptions could result in materially different conclusions. All information contained in this publication have been compiled and obtained from sources believed to be reliable and credible but no representation or warranty, express or implied, is made by Zurich Insurance Group Ltd or any of its subsidiaries (the ‘Group’) as to their accuracy or completeness.

Opinions expressed and analyses contained herein might differ from or be contrary to those expressed by other Group functions or contained in other documents of the Group, as a result of using different assumptions and/or criteria.

The Group may buy, sell, cover or otherwise change the nature, form or amount of its investments, including any investments identified in this publication, without further notice for any reason.

This publication is not intended to be legal, underwriting, financial investment or any other type of professional advice. No content in this publication constitutes a recommendation that any particular investment, security, transaction or investment strategy is suitable for any specific person. The content in this publication is not designed to meet any one’s personal situation. The Group hereby disclaims any duty to update any information in this publication.

Persons requiring advice should consult an independent adviser (the Group does not provide investment or personalized advice).

The Group disclaims any and all liability whatsoever resulting from the use of or reliance upon publication. Certain statements in this publication are forward-looking statements, including, but not limited to, statements that are predictions of or indicate future events, trends, plans, developments or objectives. Undue reliance should not be placed on such statements because, by their nature, they are subject to known and unknown risks and uncertainties and can be affected by other factors that could cause actual results, developments and plans and objectives to differ materially from those expressed or implied in the forward-looking statements.

The subject matter of this publication is also not tied to any specific insurance product nor will it ensure coverage under any insurance policy.

This publication may not be reproduced either in whole, or in part, without prior written permission of Zurich Insurance Group Ltd, Mythenquai 2, 8002 Zurich, Switzerland. Neither Zurich Insurance Group Ltd nor any of its subsidiaries accept liability for any loss arising from the use or distribution of publication. This publication is for distribution only under such circumstances as may be permitted by applicable law and regulations. This publication does not constitute an offer or an invitation for the sale or purchase of securities in any jurisdiction.