Comfortingly, equity markets have been grinding higher over the last month and bond markets are stabilising after concerted efforts to increase liquidity via “buyer of last resort” facilities provided by many central banks has seen spreads decrease.

Equities are apparently looking through current earnings weakness and the looming low point in economic statistics. Clearly the most obvious trigger point for a second downward leg in stock prices is a second wave of the virus striking in one or more major economies. The latest rally was based on some promising vaccine trials by US biotech company Moderna. The operative word here is “promising”. The trial was based on eight people (no, that’s not a typo) who each received two doses of the vaccine. They then had their blood (with the newly acquired antibodies) tested in the lab against COVID-19. The impact in neutralising the virus was similar to victims who had contracted it and subsequently recovered.

While definitely a step forward, it is important to note a number of key factors impacting the timeframe in which we can all jump on a plane and travel the world again. Namely:

- This initial trial used healthy volunteers aged between 18 and 55. The efficacy on older people with pre-existing health conditions, where most deaths occur, may be far less.

- Gaining FDA approval requires a number of successful pre-clinical and clinical trials using significantly larger sample sizes which usually take well over 12 months to conduct.

- Once approved, ramping up production is a whole new challenge, especially if you are talking about the global population.

Looks like the “holiday in Australia” campaign will likely have some legs after all, particularly in the next 12 months.

What about bond yields? Forget lower for longer, it looks more like lower forever. The RBA timetable for raising interest rates is not even on the horizon given they continue to target a 3 year bond yield of 0.25%, the same as overnight cash. With inflation likely well below the target range of 2-3%, the only clear argument for higher interest rates over the next few years is debt.

Governments around the world (most of which started with huge debt loads pre COVID-19) have deliberately engineered a huge uplift in debt to try and minimise the impact of the virus on their populations and economies. There are only three ways to reduce / eliminate debt: gradually repay it, get the lender to forgive the debt or finally inflate it away. The third option is by far the most palatable. Just one problem - you need to engineer some inflation to reduce the real value of the debt. If successful, interest rates would inevitably rise as well.

Can this happen? It’s not inconceivable over time if you think about the factors which have driven the great deflation. First among these are cheap imports from China. Given the trade tensions emerging between many western countries and China, it is safe to say this trend is now in jeopardy. Adding to this nascent trend is the Five Eyes robot screaming “Danger Will Robinson, alien approaching!”; or perhaps more accurately “danger already here”... A report to the Five Eyes spy network (US, Britain, Australia, Canada and NZ) identified that of this group Australia had the highest number of strategic products and processes which were dependent on China - over 500. Breaking these supply chains will inevitably mean higher prices - the cost of security for critical goods like medical supplies, chemical inputs into drugs and the like (I emphasise that toilet paper does NOT fit into this category as the mountains of stock now in supermarkets attests).

Fortunately, Australian Federal Government net debt was circa 30% of GDP pre COVID-19 and is likely to rise towards 40% in the brave new world – though this could end up being considerably less given the over-estimation in the JobKeeper take up. This is low by world standards and while it may see us lose our AAA credit rating, this is unlikely to be a big deal. So, as a nation we still have the option to repay the debt rather than try and inflate it away. This brings us back to an earlier assertion - don’t expect higher interest rates in the next couple of years.

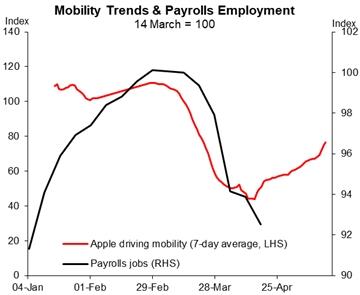

Green Shoots in Economic Activity

Anyone aged say 45 and under has never experienced a genuine recession in their working life. And nobody has ever experienced anything as large and pervasive as the JobKeeper subsidy programme. While we are yet to see the bottom in traditional economic statistics, pleasingly some leading indicators are already suggesting a bounce in activity. Mobility trends from Apple (yes, you are being watched) indicate that people are increasingly on the move – driving, walking or taking public transport. Outings all generate economic activity and, with a lag, employment.