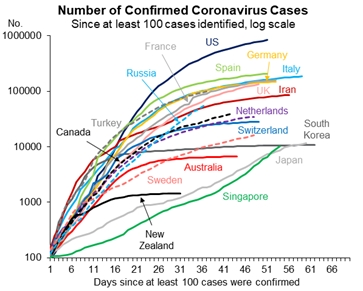

The accountants amongst you will be familiar with the acronym FIFO (First In First Out). This is equally applicable to China when we are talking about COVID 19, where most lock down restrictions have been lifted after 11 weeks of immense economic pain. For Q1, GDP fell 6.8% - a fall in activity unmatched since the 1970’s.

This was a Big Bang exit strategy. Is this too soon? Maybe, but it is important to remember that the system of government in China allowed much more severe restrictions than are possible in most western economies. To give an example, the current debate in Australia about getting people to sign up to COVID tracking software did not occur in China. It was mandatory, as is temperature testing when entering retail spaces. This is far more difficult to implement in western economies where individualism is king. Witness the lock down demonstrations in several US states and the fines issued in Australia for ignoring social distancing protocols. It is far more likely that the exit strategy in most western economies including Australia will be staged rather than a Big Bang approach, and the China timeframe of 11 weeks from whoa to full steam ahead will likely be stretched. This has a serious negative impact on short term economic activity for the remainder of 2020. GDP in Australia will probably be -4 or 5% for calendar 2020, and unemployment will touch 10/15% depending on how generous you are at counting JobKeeper recipients. 2021 will see sharp improvement, but not to the levels pre COVID.

The current notices for Australian states and territories to BEGIN lifting restrictions are shown below.

Timeline of Government restrictions

| Location |

Current Government Effective Dates for Restrictions (subject to change) |

| New Zealand |

27 April 2020 (level4) then from 11 May (level 3) |

| NSW | 29 June 2020 |

| VIC | 11 May 2020 |

| QLD | 19 May 2020 |

| ACT | 7 July 2020 |

| WA | 30 April 2020 (expect to be extended in some form) |

| SA | 2 May 2020 (expect to be extended in some form) |

| TAS | 11 June2020 |

Australia’s relatively mild run in with COVID 19 compared with many other countries has prompted the Chief Medical Officer to begin talking publicly about exit strategies. This is dependent on more testing, better contact tracing (presumably via the optional sign up to the mobile phone app) and enhancing the medical response to local outbreaks. As suspected a gradual and staged approach was flagged, with some restrictions possibly being lifted in 3 weeks or so. These may include some community sport and allowing slightly larger gatherings, but not large gatherings (e.g. sports crowds, clubs, etc) and definitely not international travel.